Federal Debt: More Than You Want to Know

Source: FRED

Recently David Sacks, a Silicon Valley investor who is now Donald Trump’s AI and crypto czar (gag me with a blockchain), raised an interesting question about federal debt.

True, he did so in the course of saying something really stupid. Are tech bros even more arrogant and ignorant when they make pronouncements about the federal budget than they are on other topics, or does it just seem that way to me because I know something about the subject? Still, a good question is a good question, no matter who asks it or why.

So here was Sacks’s pronouncement:

s_!BZ1x!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F6f488f39-cb90-4800-ba51-ad0f210b2679_1176x578.png)

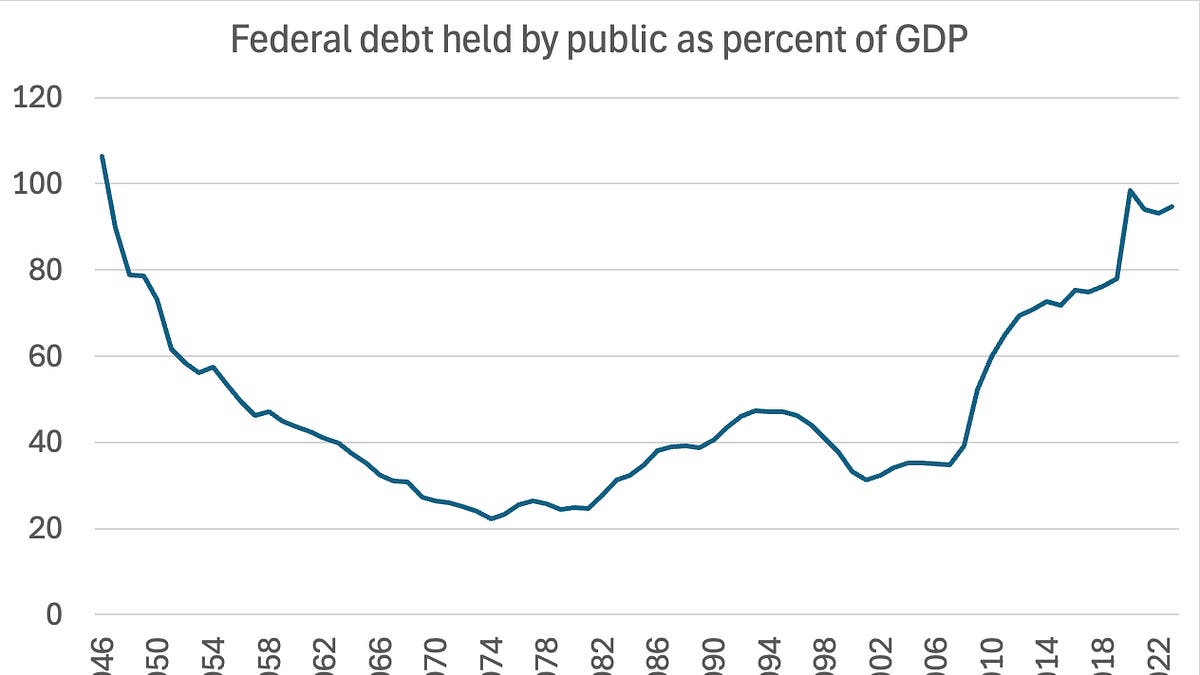

If he actually did ask where the money went, any random economist would tell him that detailed historical budget information is available from both the Congressional Budget Office and the Office of Management and Budget. (Hint: We didn’t spend the money paying Social Security to dead people.) But as the chart at the top of this post shows, he’s not wrong in saying that we have World War II levels of indebtedness.

So how did we get here? What could/should we have done differently? What should we do in the years ahead?

Beyond the paywall is a sort of primer, like the one I did on tariffs. It will cover:

-

The effects of deficits and debt

-

The reasons it sometimes makes sense to run budget deficits and hence run up public debt

-

The specific reasons debt increased a lot after the global financial crisis of 2008, and whether there was any good way to have avoided that rise

-

What we do now, and why we’re unlikely to do it

Not to be coy, most of the run-up in debt over the past 25 years actually took place for good reasons, and it’s hard to tell a story in which we ended up with substantially less debt without paying a heavy price in high unemployment. But we are now at a point where continuing to run up debt no longer makes sense. Even people like me, who are usually relaxed about debt, would really like to see a serious effort to slow the rate at which debt is rising. And under current conditions we could rein in the growth in debt without doing major economic damage if politicians — especially Republicans — were willing to act responsibly.

But they aren’t.

Does debt matter?

In fiscal 2024 — which ran from Oct.1 2023 to Sept. 30 2024 (don’t ask) — the federal government spent $6.75 trillion while collecting only $4.92 trillion in revenues. So it ran a deficit of $1.8 trillion. It covered that gap by selling bonds, so we ended up with a debt to the public of \(28 trillion. To say the obvious, don’t confuse the deficit, which is a yearly amount, with the debt, which is the total amount of the country’s indebtedness at a particular point in time. You’d be amazed how many times I’ve found myself in discussions where it eventually becomes clear that people are mixing up these two concepts. All of these numbers are almost inconceivably large. But do they matter? Deficits clearly do matter. Other things being the same, a bigger government deficit leads to higher spending in the economy as a whole. This can happen directly, if the government itself buys more stuff; it can also happen indirectly because consumers’ income rises, either because the government gives them money (as in the Covid stimulus checks) or because the government cuts their taxes. Is a deficit-driven increase in total spending a good thing or a bad thing? It depends on the state of the economy. In a depressed economy deficit spending can help reduce unemployment and foster recovery. In an economy at full employment, deficits can feed inflation, drive up interest rates, and crowd out private spending. More on that in a bit. What about the level of debt? Does it matter as well? You might assume that it’s always bad to have high levels of government debt. But many arguments about why you should worry about the debt end up being somewhat circular — for example, claims that debt is a problem because it hurts confidence, that is, debt is bad because investors will think it’s bad. To the extent that we do worry about the level of debt, we should always be clear that what matters is the level relative to the government’s tax base, which in modern nations is basically the whole economy. That is, to the extent that the level of the debt matters, what really matters is debt as a percentage of GDP. Since GDP normally grows over time, this in turn implies that governments never have to pay off their debts; at most they need to keep their borrowing low enough that debt grows more slowly than GDP. That is, governments need to maintain a sustainable debt path. A case in point: How did America pay off its debts from World War II? It didn’t: s_!dZoB!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fe705369a-29b2-4f53-b715-cb85ef420add_1064x688.png)

The blue line shows federal debt in billions of dollars (left axis), which was higher at the end of the Eisenhower administration than it had been in 1946. The red line shows debt as a percentage of GDP (right scale), which fell steadily thanks to a combination of real growth and moderate inflation.

So we never paid off our war debt. We did, however, run small enough budget deficits that debt came way down as a percentage of GDP, and remained at non-alarming levels up through 2007.

Since then, however, we’ve run big deficits and driven the debt/GDP ratio back to a level typically associated with the aftermath of war. Why? Before I answer that question, we first need to examine the circumstances when deficit spending is good.

When deficits are good

There are some people who believe, or claim to believe, that the federal budget should always be balanced. But serious economists know better, and have known better for more than two centuries.

The original pro-deficit argument came from the early 19th-century economist David Ricardo, who argued that large but temporary surges in spending — typically but not necessarily wars — should be paid for in large part by borrowing rather than taxes. Why?

Ricardo’s point was that to pay for a major war out of current revenue would require very high tax rates. Such high rates would create incentives for large-scale avoidance and evasion. That is, people would either stay away from easily taxed activities or try to hide their incomes from the government. Both would have substantial economic costs.

So it would be better, he argued, to raise only enough tax revenue to partly pay for the war, borrowing the rest, but keep taxes elevated for a while after the war to help pay down the war debt (or, in a modern context, to allow debt to fall as a percentage of GDP.)

This is, in fact, what you see if you take a very long view of British government debt:

Source: Bank of England

Notice, by the way, just how high those peaks are. Historically, stable governments have been able to borrow a lot without experiencing a debt crisis.

So wars and other emergencies are one reason to run big budget deficits, even if they lead to higher debt. There is, however, another reason to run budget deficits: to boost a depressed economy by increasing overall spending.

If there were any doubts that increasing deficits can boost a depressed economy, and conversely that trying to reduce deficits can deepen a depression, those doubts should have been ended by the euro crisis of 2009-13. A bond market panic forced some but not all European countries into severe austerity policies, slashing spending and in some cases raising taxes. And the deeper the cuts, the worse an economy performed.

So there’s a case for running deficits and increasing debt when the economy is depressed. How does that relate to the big debt increases after 2007?

*From the financial crisis to Covid*

The collapse of the 2000s housing bubble and the financial disruptions that followed sent the U.S. economy into a protracted slump, the worst since the 1930s. You can measure that slump many ways, all of which tell the same story. Here’s the employed percentage of adults 25-54:

s_!R3_p!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Faa05b8cf-05f0-47fb-a9ed-5faf0cb1b15c_1060x672.png)

Since deficit spending helps boost a depressed economy, it made a lot of sense to run substantial deficits after 2007. In fact, given that recovery was much slower than it should have been, you could (and I would) argue that the deficits should have been even bigger.

But wait. Aren’t there other things you can do to perk up a depressed economy? Normally, yes — but not this time.

Usually, the main way we fight recessions is by having the Federal Reserve print money — or, to be more accurate, increase the monetary base, the sum of currency in circulation and reserves held by private banks, by buying bonds from those banks.

When the Fed does this, banks usually lend the money out, which drives interest rates down and leads to higher investment, consumer borrowing, and so on. And there’s a lot to be said for having the Fed fight recessions: It’s easy, it doesn’t requite legislation, and of course it doesn’t add to the national debt. So expansionary monetary policy is the routine response to a depressed economy — sort of the over-the-counter painkiller of macroeconomics.

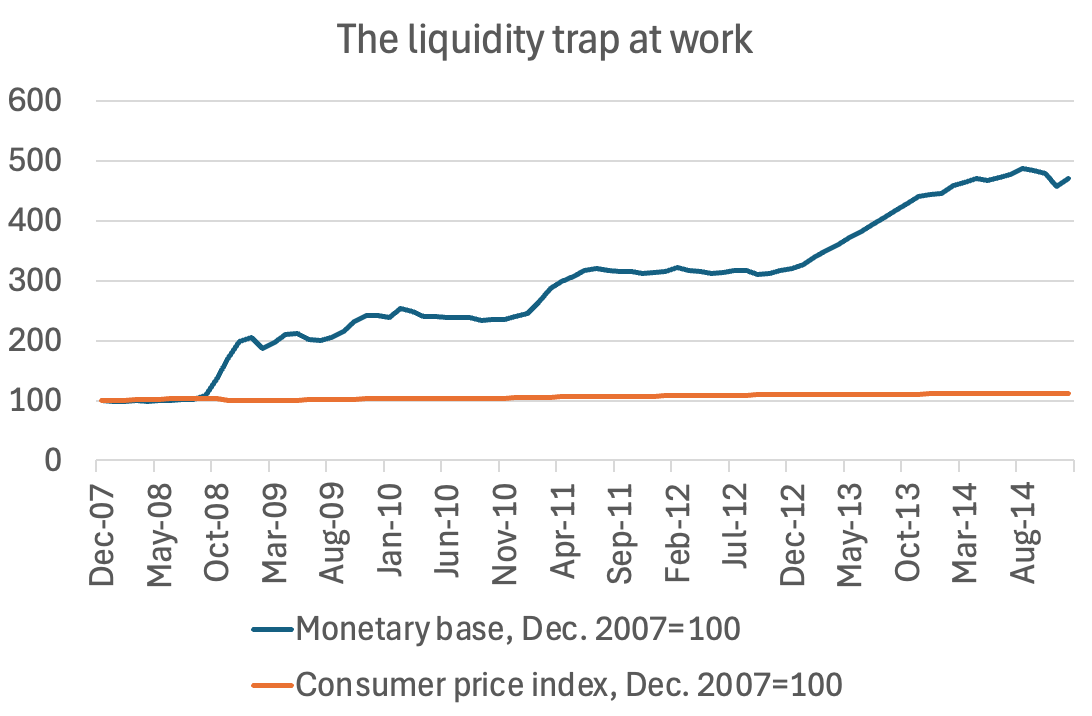

But there are limits to how much the Fed can do. It can push interest rates down more or less to zero, but at that point it loses traction: it can print as much money as it likes, but banks have no incentive to lend it out at near-zero interest rates, so the money just sits there. This is the infamous “liquidity trap” (again, don’t ask) that prevailed during the 1930s, reemerged in the 1990s in Japan, and became reality throughout the advanced world after 2008.

The Fed did what it could, printing a lot of money, amid dire warnings that this would unleash inflation. But as I could have told the critics (and did), this wasn’t going to happen:

Source: FRED

Unfortunately, while the Fed’s actions didn’t cause inflation, they also didn’t do much to help the economy, which remained depressed for a long time. As a practical matter, deficit spending was the only game in town. Indeed, without those deficits the financial crisis could have turned into a full replay of the Great Depression.

So we were right to run up debt after 2007. In fact, we should have run up even more debt, to get back to full employment sooner.

By 2019 we were, finally, more or less back to full employment. But then Covid struck.

In the early stages of the pandemic, before we had vaccines or even a good understanding of how the virus spread, the only way we knew to limit the death toll was to limit face-to-face interaction, which meant shutting down large parts of the economy. As I put it at the time, we put the economy into a medically-induced coma.

But this meant depriving many Americans of the ability to earn a living; you can see the plunge in the prime-age employment rate above. How we were to protect workers and their families from extreme financial hardship?

The answer was government aid, mainly taking the form of stimulus checks and temporarily expanded unemployment benefits. This surge in emergency spending was, you might say, the fiscal equivalent of war. And Covid-related aid accounts for that last uptick in debt in the chart at the top of this post.

Could or should the aid have been less generous? Maybe; there has been a lot of criticism of the scale of the second round of aid at the beginning of the Biden administration. But even if total aid had been, say, a trillion or two smaller, we’d still have debt close to 1946 levels.

So could or should we have avoided the big run-up in debt after 2007? If we’d tried to run smaller deficits after the financial crisis, we would have suffered even higher unemployment and experienced an even slower recovery. If we’d stinted on aid during the pandemic, we would have added a lot of financial pain to the havoc wreaked by disease and death.

You can quibble over the details of policy, but at a basic level we borrowed heavily to cope first with an economic emergency, then with a health emergency, and there was no good way to avoid a large rise in debt.

The real question should be, now what?

The future that should be, but won’t

America in 2025 is not experiencing a pandemic (although I’m keeping an eye on bird flu.) Nor do we have a depressed economy with near-zero interest rates; the Fed has raised rates a lot to fight inflation, which means that deficits are crowding out private spending.

At the same time, debt is still growing faster than GDP, even though we’re at full employment, and with interest rates on debt much higher than they were for most of the era after the financial crisis, the growth of debt is more worrisome than it would be if rates were still close to zero.

So now would be a good time for fiscal orthodoxy to get us back on a sustainable debt path. If Congress and the White House could agree on some combination of tax hikes and spending cuts that would greatly reduce the deficit, the Fed could offset the negative effect on spending by cutting interest rates, and everyone would breathe a little easier.

Also, if wishes were fishes, beggars would ride, or something like that.

The G.O.P. now controls all three branches of government, and is dead set against any tax increases other than tariffs, which won’t yield much revenue. In fact, Republicans are determined to give wealthy Americans another big tax cut, which will supposedly be offset with spending cuts — and no, laying off critical federal workers, including the people at the IRS responsible for going after tax cheats, won’t do the trick.

Remember, the federal government is basically an insurance company with an army: defense, Social Security, Medicare and Medicaid account for the bulk of noninterest spending. Everyone considers cuts to Social Security and Medicare politically off-limits, so Republicans are proposing savage cuts to Medicaid. They’re about to find out that making deep cuts to a program that insures 70 million Americans isn’t that easy, either.

So where we are now is that for the first time since 2007 the economic situation really would allow us to make a serious effort to reduce deficits and maybe even the ratio of debt to GDP. But given the political situation, that’s a fantasy.

Write a comment