The Economics of Stagflation, Part III

Item: On Aug. 28 Chris Waller, a member of the Federal Reserve’s Board of Governors — and rumored to be in the running for the Fed’s next chair — gave a speech warning about economic weakness:

Returning to the labor market, risks are continuing to build. In my July 17 speech, I said that private-sector job creation was nearing stall speed, and the data received since then have put an exclamation point on this statement.

Clearly, it’s time to cut interest rates, to get ahead of the looming slowdown!

Item: On the same day, the Wall Street Journal reported strong indications that inflation is about to accelerate:

s_!-Xfd!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F4ee7b2c0-a95c-49f1-a967-d21b31a9b896_800x450.png](https://substackcdn.com/image/fetch/\(s_!9GXp!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F84058b97-4435-42f1-9d68-1d247df14a0f_1270x308.png)

Clearly, this is no time to cut rates! If anything, the Fed should be prepared to raise rates if inflation rises substantially.

Sometimes the state of the economy offers clear guidance on what policies should be undertaken. And, in the short term, the policymakers who make those decisions are at the Federal Reserve. Yes, fiscal policies – taxes and government spending – also have significant effects on the economy. But fiscal policy is slow to change – typically, it requires passing legislation. In contrast, the Fed can have an immediate effect on the economy by lowering or raising the *Federal Funds rate* – the short-term rate that the Fed has direct control over. Since fiscal policy can only be implemented with long time lags, it’s basically the job of the Fed to keep the economy on an even keel.

When the inflation rate is low but the unemployment rate is high, as it was during the Great Recession in the aftermath of the 2008 financial crisis, the Fed should cut the federal funds rate. By lowering the fed funds rate, the Fed makes it cheaper for banks to lend. This boosts the spending and investing activity in the economy and brings unemployment down.

When inflation is high but unemployment is low – that is, when the economy is at risk of overheating -- as it was in 2022, the Fed should raise the fed funds rate. This slows down spending and investing and brings inflation down.

But when the unemployment rate and the inflation rate are both too high — what economists call “stagflation” — the Fed faces a dilemma. Cut the fed funds rate ~rates~ to support employment and you risk worsening inflation. Raise the fed funds rate to fight inflation and you risk raising unemployment. With stagflation, there are no easy answers, just a tradeoff of risks.

And this dilemma looks very relevant right now: many economic indicators suggest that the United States will soon undergo at least mild stagflation.

In this final primer on stagflation, I’ll talk about policy responses to stagflation. Beyond the paywall I’ll discuss:

1\. Stagflation policy dilemmas: Theory and historical experience

2\. Why we have an independent Fed, and the paramount importance of Fed credibility

3\. Consequences of Donald Trump’s assault on the Fed

*Stagflation Policy Dilemmas*

The term stagflation was introduced in Britain during the 1960s and has repeatedly been a problem ever since. Whenever both the unemployment rate and the inflation rate are high, central banks — the Fed in the United States — have to make a judgment call about which is the greater evil.

If you prioritize fighting unemployment, inflation may soar. It may even become entrenched in the economy, as happened in the US during the 1970s. As I explained last week and as illustrated by the Fed-induced recession in the 1980s, getting inflation under control once it has become entrenched can be very costly, requiring high interest rates and high unemployment.

But if you prioritize fighting inflation, you may impose high unemployment on the economy. This inflicts severe suffering on the jobless, as well as costing the economy large amounts in terms of lost goods and services.

It’s depressingly easy to come up with examples in which central banks made the wrong call and inflicted significant gratuitous damage in the process.

In the United States, the most famous example of ignoring inflation risks while focusing solely on unemployment comes from the Nixon years.

When Arthur Burns became Federal Reserve chairman in 1970, the U.S. economy was in the midst of stagflation. Along with a recession (the shaded area in Chart 1) it was also experiencing high inflation (the dashed line in the chart), running at around 6 percent. Under intense political pressure from Richard Nixon, Burns chose to believe that the high inflation reflected temporary factors that would soon go away, and pushed for sharp reductions in the Federal Funds rate (the solid line in Chart 1.)

s_!-Xfd!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F4ee7b2c0-a95c-49f1-a967-d21b31a9b896_800x450.png){kind=link}

Chart 1

For a short period of time Inflation did come down but then it shot right back up. Burns has become the poster child in economics lore of what not to do as a Fed Chairman – that is, give in to political pressure and allow high inflation to become entrenched, so that the U.S. economy eventually had to pay a huge price to get it back down.

A classic example of making the reverse mistake was the European Central Bank’s decision to hike interest rates twice during a period of mild stagflation in 2011. Euro area inflation was running somewhat above the ECB’s 2 percent target, although not by a large amount — it peaked at 3 percent. And most of this rise in inflation reflected clearly temporary factors, mainly a rise in world oil prices as the global economy recovered from the 2008 financial crisis.

At the same time, much of Europe was in the midst of a serious economic crisis, with concerns about government solvency leading to very high unemployment in much of southern Europe. Yet the ECB decided that it had to appear tough and its inflation target was sacrosanct. As a result, its interest rate hikes deepened the crisis. A few months later, when it became obvious that the ECB had severely miscalculated, it reversed those hikes.

Why do policymakers make mistakes like this? One answer is simply that making policy in the face of stagflation is inherently difficult, with no good answers. So mistakes will inevitably happen. But another answer is politics: central banks can give in to political pressure and be too lenient, or they can be too tough in an attempt to forestall the appearance of caving into political pressure.

The political pressure to be too lenient is easy to explain. Other things equal, low interest rates and a booming economy are good for whoever currently holds power. So, without proper firewalls between political leaders and the central bank, political leaders are inevitably tempted to pressure the central bank to keep interest rates low. What about the risk of higher inflation? Politicians will typically consider that a problem to deal with after the election. Or they may listen to self-serving advisers who tell them what they want to hear: that inflation won’t be a problem and that those pesky economists have it all wrong.

Indeed, we know that Richard Nixon exerted a lot of pressure on Burns to keep the fed funds rate low. Moreover, there have been much more extreme examples in other countries. Most recently, President Erdogan of Turkey, which is a democracy on paper but an autocracy in practice, went all in on heterodox monetary theories that justified keeping interest rates low even as inflation accelerated, and didn’t back down until inflation hit 80 percent.

Political interference in monetary policy can be greatly limited, although not necessarily eliminated, by giving central banks substantial independence~.~ This is why Donald Trump’s attack on the Fed is tantamount to a five-alarm fire. More on that later in this post.

Correspondingly, central bankers can err on the side being too tough because they are trying to assert their independence from politics. Paul Volcker is regarded as a heroic figure for seeing the United States through the pain of disinflation in the 1980s. Ben Bernanke, in contrast, kept the fed funds rate extremely low and kept the money flowing after the financial crisis despite constant pressure from people warning that he was “debasing” the dollar. In retrospect, Bernanke deserves but doesn’t get comparable acclaim.

So when proper firewalls are absent, politicians tend to pressure central bankers to ignore inflation. And in reaction, central bankers – such as the ECB in 2011 — can have a bias toward overemphasizing inflation risks and not caring enough about full employment.

To err is human, so central banks, which are run by human beings, will make mistakes. However, both the size and the negative consequences of these mistakes can be reduced by making sure that central banks are insulated from political pressure and use their independence to acquire and maintain credibility.

The importance of Fed independence

In almost all wealthy nations and many middle-income nations, short-term interest rates like the Federal funds rate are set by independent central banks. That is, at the Fed and its counterparts’ interest rate decisions are made by technocrats rather than dictated by politicians. The Fed is ultimately accountable to elected officials: Fed governors must be appointed by the president and approved by Congress. But they are traditionally chosen for their professional expertise, not their partisan loyalty, and they are insulated from short-term political pressure by receiving long-term, 14-year appointments. Donald Trump’s attempt to fire Lisa Cook is the first time a president has ever tried to remove a Fed governor before their term expired.

Why grant the Fed so much independence? The immediate answer is that Fed independence limits the scope for irresponsible policy. As I noted at the beginning of this post, fiscal policy — changes in taxes or government spending — requires that Congress pass legislation, which takes time and also provides an opportunity to put the brakes on a president who wants to goose the economy before an election, or who simply has crazy policy ideas. The Fed funds rate, by contrast, can be changed at a moment’s notice, without legislation. Literally, all it takes is a phone call to the desk at the Federal Reserve Bank of New York that manages the execution of fed funds rate changes. As the sorry tale of Richard Nixon and Arthur Burns shows, as well as the recent experience of Turkey where a politicized central bank resulted in 80% inflation, it’s important to protect the independence of the Fed in order to assure the stability of the economy and financial markets.

And the story doesn’t end there. In the United States, in the four decades since Paul Volcker asserted the independence of the Fed – at a high cost to the economy of years of stagflation and high unemployment – the Fed has accumulated a deep reserve of credibility with investors, financial markets, and the general public. As a result, when making economic decisions about the future, Americans have come to believe that, whatever may happen in the short term, the Fed will do whatever is necessary to keep inflation under control in the long run. This credibility, in turn, has major benefits for effectively managing the economy.

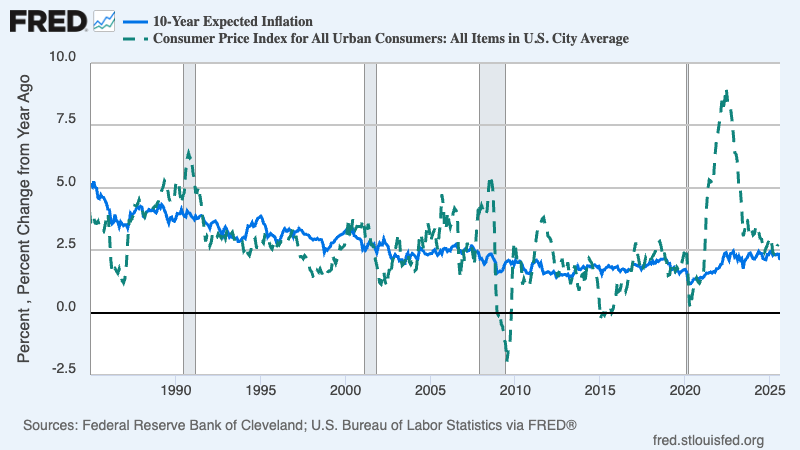

To show what I mean about Fed credibility, the solid blue line in Chart 2 shows an estimate, produced by the Cleveland Fed, of average private-sector expectations of inflation over the next 10 years:

{kind=link}

Chart 2

As you can see, long-run inflation expectations have been low and stable since the Volcker disinflation of the 1980s. This has been true even though the actual rate of inflation, shown by the green dashed line, has fluctuated a lot. This stability of long-run expectations is a consequence of the Fed’s credibility. In other words, although consumers and firms may perceive an uptick in inflation in their day-to-day lives, the credibility they invest in the Fed leads them to believe that the Fed will eventually get inflation under control. As a result, they don’t begin demanding higher wages and prices. When this happens, economists say that inflation expectations are “anchored”. (I covered the meaning of anchored inflation expectations in last week’s primer.)

So anchored inflation expectations are a result of the Fed’s now long-standing credibility in fighting inflation. What are the advantages of this credibility?

First, it helps us avoid entrenched inflation. As we saw in Part I of this primer, the stagflation of the 1970s was very difficult to cure because inflation had become entrenched in the minds of Americans. In other words, inflation had become self-sustaining, driven by a combination of catch-up to past inflation and expectations of future inflation. In order to bring inflation down and re-establish Fed credibility, the Volcker Fed had to inflict years of high unemployment and high interest rates.

The belief that the Fed won’t allow that to happen again has been powerful protection against a repeat performance. As a result, we haven’t had to worry that a temporary uptick in inflation will cause inflation expectations to become unanchored and lead to runaway, embedded inflation.

Look again at Chart 2. Toward the right of the chart you can see the inflation surge of 2021-22, largely caused by Covid-related disruptions of supply chains. The striking thing about this surge, in retrospect, is how easily it dissipated. Inflation never became entrenched: it fell rapidly as supply chains unsnarled, without the need to put the economy through a period of high unemployment. As a result of the Fed’s hard-worn credibility, Americans felt assured that the Fed would eventually get inflation under control. Inflation expectations remained anchored, and the country benefited from a painless disinflation as supply chains returned to normal.

The second benefit of Fed credibility is that is allows the Fed to avoid overreacting to what are clearly temporary inflation upticks. Chart 2 shows an inflation surge in 2008 and another, smaller surge in 2011. As I mentioned earlier in this post, when discussing the mistakes of the European Central Bank, the Fed knew that in both these episodes that inflation was up due to fluctuations in oil prices. Resting upon their deep reserve of credibility, the Fed was able to “look through” these temporary upticks and leave interest rates unchanged without the fear that inflation would become embedded in the minds of the public.

So while the Fed isn’t always right, the credibility of an independent Federal Reserve has been a huge help in maintaining the stability of the US economy.

Which leads to a final subject: The threat Trump now poses to that hard-won credibility.

The threat from Trump

Dealing with stagflation is always difficult. Navigating an economy with rising inflation driven by tariffs and deportations and weakening growth caused by policy uncertainty would be extraordinarily tricky even in the best of circumstances.

But these aren’t the best of circumstances, for Donald Trump has chosen this moment to make an unprecedented assault on the Fed’s independence. We’ll soon learn more about whether he will succeed in firing Lisa Cook, a member of the Fed’s Board of Governors, but the Cook affair is obviously part of a concerted effort to take interest rate policy out of the hands of technocrats and put it in the hands of the White House.

As I’ve explained, there are two big reasons we don’t want to do that. First, politicians may abuse monetary policy for short-run political gain. Second, politicians may take economic advice from cranks who tell them what they want to hear.

Trump epitomizes both dangers. In particular, we don’t need to wonder whether he’ll try to impose crank economics. He has already declared that he wants the Fed funds rate to be reduced by 300 basis points — a huge cut, something we normally do only when the economy is in deep crisis. Yet his claim is that the economy should be rewarded with huge rate cuts because, he says, it’s doing so well. This is crazy and irresponsible.

As we’ve just seen, economic policy in the United States has benefited greatly from the Fed’s hard-won credibility. If Trump takes over, that credibility will quickly disappear.

In fact, a Trump takeover might well have a perverse effect on interest rates. He could cut short-term rates, which the Fed effectively controls, for a while. But look back at Chart 1. Arthur Burns managed to cut the Fed funds rate for a while, but rising inflation soon forced him to raise rates well above their starting point.

And long-term rates, such as mortgage rates, are largely determined by expectations about future inflation. We’re already seeing an unusually large spread between short-term and long-term rates. So it’s quite possible that a Trump takeover at the Fed would cause long-term rates to rise rather than fall. And long-term interest rates, not the Fed funds rate, are what matter to most people.

I began this three-part primer two weeks ago by emphasizing the stagflationary risks from tariffs and deportations. Those risks are still as great as ever. But Trump’s rapidly intensifying assault on the Fed may be the biggest risk of all.

Write a comment