The Economics of Smoot-Hawley 2.0, Part I

The Aug. 1 deadline has come and gone, and Donald Trump hasn’t made any trade deals. What some gullible reports call “deals” are at best “frameworks” in which other countries have suggested — without signing anything — that they’ll do things that might help the U.S. economy. For the most part even these understandings are vaporware. For example, the European Union [literally has no way](https://paulkrugman.substack.com/p/fossil-fool) to deliver the increased U.S. investment and increased imports of U.S. energy the Trump administration has trumpeted as part of the so-called deal.

What we’re left with is that the United States has, for all practical purposes, unilaterally imposed high tariffs. So you should think of Trump’s trade policy as the second coming of the 1930 Smoot-Hawley tariff, effectively reversing the results of 90 years of trade liberalization. In fact, average U.S. tariffs, which were very low just a few months ago, are roughly back to Smoot-Hawley levels.

Unless the courts rule Trump’s tariffs illegal — which they clearly are, but I fully expect the Supreme Court to uphold them anyway — Smoot-Hawley 2.0 is the new normal.

How should we think about this astonishing policy reversal? Beyond the paywall I’ll discuss the following issues:

1\. Where we now stand on tariffs, with historical context

2\. The likely impact of tariffs on U.S. and world trade

3\. The effect of tariffs on U.S. growth. Spoiler: significantly negative, but maybe not as bad as you imagine. But big costs for families.

I’ll follow up next week with some of the larger implications of Trump’s tariffs. Crucially, what Trump is really waging is mostly a class war against middle- and lower-income Americans rather than a trade war against other countries. The hit from his tariffs to the typical family is much bigger than the hit to GDP. Also, it’s important to understand that all of Trump’s tariffs violate solemn agreements — agreements ratified by Congress — that the United States has made in the past. So the Trump tariffs have inflicted massive and possibly irreparable damage on U.S. credibility.

*Trump Tariffs: Where we stand now*

When Trump announced his huge “Liberation Day” tariffs on April 2, many of the analysts I follow believed that they were largely a negotiating ploy. Trump, they thought, would extract concessions from our trading partners — or at least claim to have extracted concessions — and then bring the tariffs down substantially. Treasury Secretary Scott Bessent suggested that implementing a “higher tariff level” on countries would put “pressure on those countries to come with better agreements.”

I was always doubtful of this rationale because it was never clear what countries were supposed to concede, given the fact that most of our major trading partners already had very low tariffs on U.S. goods. The EU, for example, levied an average tariff of only 1 percent on U.S. nonagricultural exports. We had free trade agreements with Canada, Mexico, and South Korea! So it was clear to me that Trump wanted high tariffs for their own sake and not for any plausible bargaining purposes.

Where are we now? We have reached Trump’s self-imposed deadline, and tariffs remain very high. So much for tariffs as negotiating leverage. Even trading partners that have reached supposed deals, like the EU and Japan, are facing 15 percent tariffs.

Will the tariffs ever come down? There is still the distinct possibility that the courts will rule most of Trump’s tariff policy illegal — which in my view it clearly is. The Court of International Trade, which has jurisdiction in these matters, ruled in May that much of Trump’s tariff policy is illegal. But its judgment was put on hold while the administration appealed. It looks as if Trump will [lose this round](https://www.piie.com/blogs/realtime-economics/2025/trump-tariffs-and-courts-round-2), too. But then, as I understand it, the case will be kicked up to the Supreme Court. And nothing we’ve seen so far from the Supremes suggests that — despite the clear intent of the law — they will uphold any limits on Trump’s power.

So the tariff regime we are in now is probably where we’ll be for a long time. Specifically, we have gone from an average pre-Trump tariff rate barely above zero to a current rate roughly comparable to rates just after the 1930 Smoot-Hawley tariff:

s_!w7KM!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F4d6f058e-ca43-41c2-bcc9-e69d64323797_1894x800.png)

Source: Yale Budget Lab

For those puzzled by “pre (orange) and post (blue) substitution” labels, here is the explanation. Different countries face different U.S. tariff rates. Therefore , the post-tariff mix of U.S. imports will shift away from countries that face especially high tariffs like Switzerland (??!!) toward countries that face lower tariffs like the U.K. So should we assess the effects of the Trump tariff regime by looking at the pre-Trump mix of imports into the U.S., or the post-Trump mix of imports? Standard economics says we should choose something in between. So in the following analysis I’m going to go with a basket of US imports that implies an average 18 percent Trump-imposed tariff.

The long decline in tariff rates after Smoot-Hawley shown in the graph above was the result of 90 years of international negotiations. These began under FDR, who enacted the Reciprocal Trade Agreements Act of 1934, under which the United States made, um, reciprocal trade agreements with other countries: We’ll cut our tariffs if you cut yours. After World War II this process went global, with a series of multi-country negotiations — “rounds” — taking place under the auspices of the General Agreement on Tariffs and Trade.

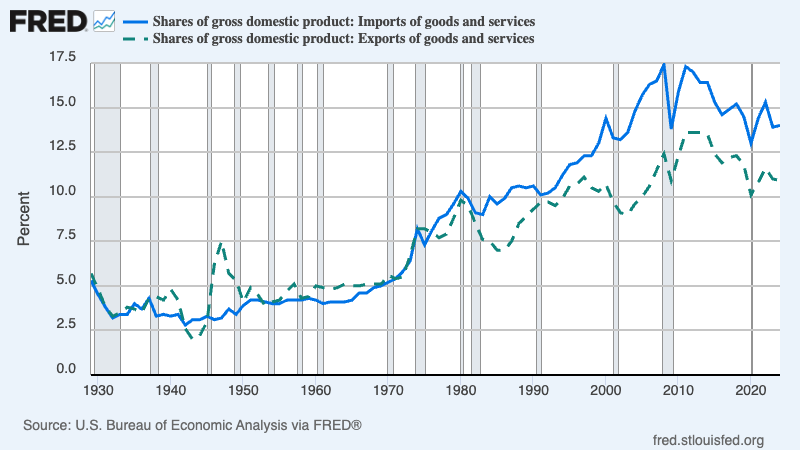

These tariff cuts enabled a huge expansion in world trade. As a result, both US imports and exports of goods and services as a share of GDP are much higher today than what they were in, say, the 1950s:

Look around your home and you’ll see imported products everywhere. While your grandparents probably made coffee with a US made old-fashioned percolator, today you have an Italian-made home espresso machine. Similarly, other countries import a lot from the U.S. – both goods and services. While the US imports more than it exports (resulting in a US trade deficit), we export much more than most Americans realize.

Trump has reversed 90 years of negotiated tariff cuts. And as we’ll see, this will lead to a large reduction in the amount of trade we do with other countries.

Who will pay Trump’s tariffs? Is it possible, as Trump claimed, that foreign exporters will “eat” the tariffs, leaving U.S. prices of imports unchanged? According to standard economics, part (but only part) of the tariffs might be absorbed by foreigners, either via foreign exporters cutting their margins or via a rise in the dollar. (A rise in the dollar means that \(1 buys more foreign goods, thereby offsetting the cost of the higher tariffs for US consumers.) But there is no sign that either of these is happening. Prices to US buyers of non-oil imports excluding tariffs (which soared during the post-Covid supply-chain crisis then plunged once the bottlenecks got resolved) have been rising slowly but steadily under Trump: s_!jh0E!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F966d75bf-df79-4093-8a4f-48bbb694da03_800x450.png)

It appears that foreigners aren’t paying any of the cost of Trump’s tariffs. Why? Part of the answer lies in the fact that the dollar has fallen, not risen — likely in reaction to the uncertainty created by Trump’s erratic policies. Another likely factor is that many of Trump’s tariffs have been levied on industrial inputs like steel and aluminum rather than on consumer goods. This raises the cost of domestically produced goods. So foreign exporters don’t need to cut their prices to compete in the U.S. market, even though they face much higher tariffs.

Given what we are observing, I will assume that foreigners aren’t changing their prices in response to Trump’s tariffs. Revisiting that assumption would have some effect on the conclusions, but it’s the best guess we can make right now.

So given that foreigners aren’t absorbing the cost of Trump’s tariffs, why haven’t we seen a more dramatic rise in prices faced by U.S. consumers? The main answer is, just wait. Many U.S. importers rushed to buy foreign goods ahead of the tariffs, and to some extent are still selling out of the stockpiles they accumulated a few months ago. Also, many U.S. companies were reluctant to raise prices and alienate customers as long as they expected tariffs to come down once Trump made his deals. For example, General Motors reports that it has already taken a [\(1.1 billion hit](https://www.bloomberg.com/news/articles/2025-07-22/gm-s-profit-falls-after-trump-tariffs-add-1-1-billion-in-costs?cmpid=eveus&utm_medium=email&utm_source=newsletter&utm_term=250722&utm_campaign=eveus) from Trump’s tariffs, which have raised its cost of production — but has not yet raised consumer prices. Now that Smoot-Hawley 2.0 appears to be here to stay, companies will begin passing on tariff costs to consumers. And once they do, consumers will begin buying fewer foreign goods. How much will the Trump tariffs shrink international trade? *The effects of Trump tariffs on U.S. trade* The chaotic rollout of Trump’s tariffs has led to wild swings in U.S. trade. And I do mean wild. As I mentioned earlier, US companies engaged in a frantic rush to front-run the tariffs earlier this year, importing a huge stockpile of goods before the full tariffs hit. These imported goods piled up in inventories. Then, once the tariffs were in place, companies slashed their imports and met a large part of consumer demand out of those inventories. Here are recent percentage changes in imports, quarter by quarter: s_!UcR_!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F1bb944fe-2dfd-412b-a080-b379e3dc4776_800x450.png)

At this point, however, much of the craziness will probably subside, as businesses adjust to a quasi-permanent regime of high tariffs. These tariffs will make imports substantially more expensive than before, leading to less trade. But how much less?

WONK WARNING. Feel free to skim or skip the next few paragraphs.

The key number is something known as the Armington elasticity. This asks the question, what happens to the relative demand for imports compared with domestic goods when the price of imports rises? Specifically, if import prices rise by one percent, by how many percent does the relative demand for imports fall?

There have been many, many, many attempts to estimate the Armington elasticity. One recent survey found 3,524 reported estimates. The average, which is also the number many estimates seem to cluster around, is about 3.

So what do I get if I assume an 18 percent tariff rate and an Armington elasticity of 3? In 2024 U.S. imports of goods were 11.2 percent of GDP. By my estimate, Trump’s tariffs will reduce this to 7.1 percent. That’s a 36 percent decline, roughly comparable to the 40 percent decline in the import share that took place between 1929 and 1932, although the story behind that decline was very different.

{kind=link}

Trump’s tariffs, then, will have a big impact on U.S. trade. But what will they do to the U.S. economy?

The cost of Trump’s tariffs

Let me get straight to it: My little model says that the Trump tariffs will reduce U.S. real GDP by 0.37 percent relative to what it would have been otherwise.

I suspect that many readers will find this number surprisingly small. So let me say that it’s not out of line with other estimates. The Yale Budget Lab, which has a much more elaborate and rigorous model, comes up with almost the same number: 0.4 percent.

Let me explain where this number comes from, then talk about why, I think, many people expect it to be bigger.

Once again, WONK WARNING. You may want to skip the next few paragraphs and just take my word for the conclusion.

OK, consider a thought experiment. Imagine slightly increasing the Trump tariffs, so as to reduce imports by an additional $100 million (that’s a small number in this context.) The US economy will save $100 million in money paid to foreigners. However, it will give up useful goods — goods consumers were willing to pay $118 million for, because they have to pay the cost of the tariff. So a tariff increase that reduces imports by $100 million actually makes the U.S. economy $18 million poorer, because we lose goods that were worth $118 million to consumers while saving only $100 million.

Now imagine getting to an 18 percent tariff in many small steps, starting close to zero. At each step the net loss from the tariff is the fall in imports multiplied by the tariff rate at that point. That’s a minimal loss if you increase the tariff from, say, 1 percent to 1.1 percent, but it gets much bigger if you go from 10 to 10.1. And if you sum up all the losses along the way to the current tariff rate, you get a total loss in GDP of approximately

Net loss = 0.5*tariff rate*fall in imports

(For those who remember their Econ 101, this is a “Harberger triangle”, which is how we typically measure the efficiency losses from taxes.)

As explained above, I find Trump’s tariffs reducing imports by 4.1 percent of GDP, with an tariff rate of 18% = 0.18. Plug that in and you get a loss of around 0.4 percent of GDP, which is also what the Yale Budget Lab, with a much more careful analysis, finds.

My sense is that given how much economists talk about the virtues of free trade and the evils of protectionism, these numbers will look surprisingly small to many readers. Partly this is because, as I’ll explain, this aggregate cost is the wrong number to look at. But I’d also point to two reasons we tend to treat tariffs as a bigger issue than they are, at least in terms of their effects on growth.

One is that anything involving global stuff sounds sexy and important. Compare the discussion of tariffs with the discussion of residential zoning. Zoning is a much less sexy topic. Would Tom Friedman have had a massive best-seller if, instead of “The world is flat,” he had written a book titled “The world has too many land-use restrictions”? But reasonable estimates indicate that the cost of excessively restrictive zoning is at least 2 percent of GDP, substantially higher than the cost of the Trump tariffs.

A second reason people may imagine that tariffs are more damaging than they probably are is that economists, being human (no, really, we are) tend to overhype their success stories. The development of the theory of comparative advantage, which shows how trade between two countries normally benefits both, was an intellectual triumph, and comparative advantage is something economists understand while most barbarians lay people, Donald Trump very much among them, don’t. So it’s natural to play up the stupidity of Trumpian tariff policy while downplaying the relatively modest impact of that stupidity on GDP.

But there’s a final important reason tariffs loom large in discussion, and should. The overall effect on GDP may be smaller than you think, but the effects on many families will be much bigger. The Trump tariffs will raise consumer prices by around 2 percent, which means that the typical family will lose the equivalent of about $2,000.

How can the typical family be hit so much harder than the economy as a whole? The answer is that for the most part Trump isn’t waging a trade war against other countries. He is, instead, waging a class war against middle- and lower-income Americans in favor of the wealthy.

I’ll explain why, and the role tariffs play in this class war, next week.

Write a comment