Inflation

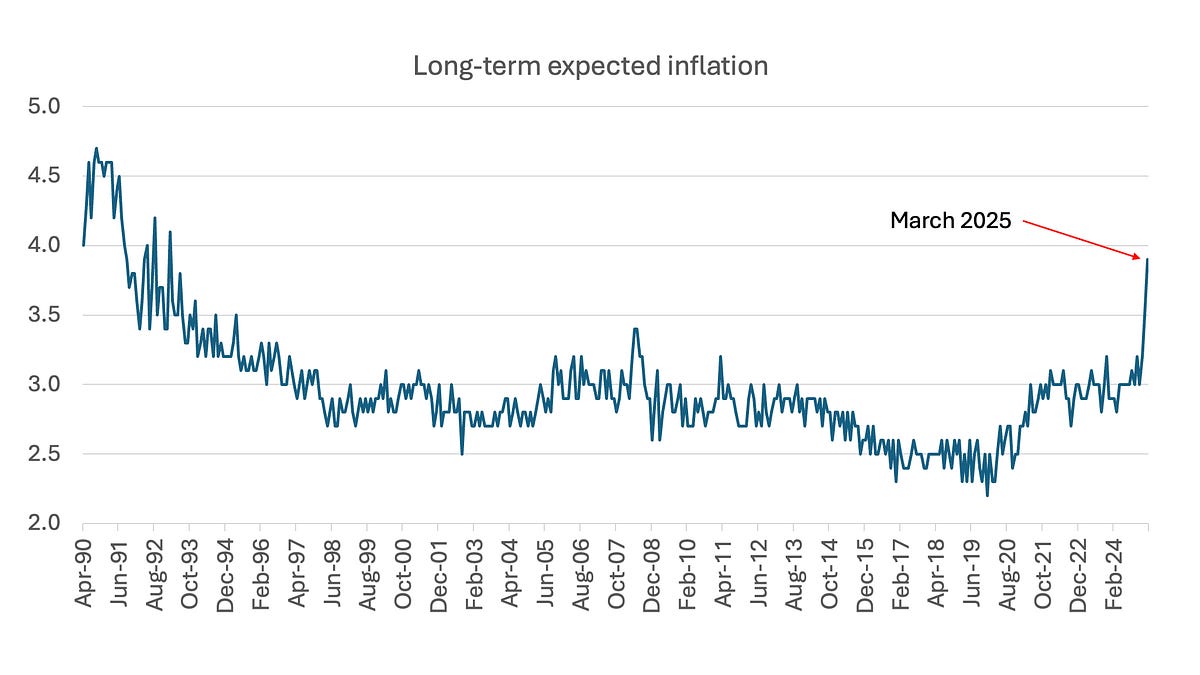

Source: University of Michigan

In 2019 the U.S. cost of living, as measured by the Consumer Price Index, was about twice as high as it had been in 1990. This may sound bad, but most Americans didn’t seem very upset. For one thing, wages were also up, and for most workers wage gains had outpaced price increases.

Also, the price increase was gradual; the average annual *rate of change* in prices — the inflation rate — was fairly low, a bit over 2 percent per year. That was low enough that people didn’t need to think much about rising prices when, say, planning family budgets. Indeed, monetary policymakers in much of the world now see inflation of around 2 percent, which is positive but low enough that people don’t spend much mental energy worrying about it, as perfectly OK, indeed better than zero inflation, because a bit of inflation, they believe, helps lubricate the economy.

Unfortunately, inflation *has* been on people’s minds for the past four or so years. Inflation shot up in 2021-22, which came as a rude shock after decades of low inflation. Even though inflation subsided over the next two years, the reaction to that shock still played a key role in the 2024 election of Donald Trump, who promised to bring prices back down again.

That promise, however, was never credible. Instead, Trump’s policies seem to be setting us up for another inflation surge, and fears of such a surge appear to be a major reason for [plunging consumer sentiment](http://www.sca.isr.umich.edu/). As the chart at the top of this post shows, consumers’ expectations of long-term inflation, as measured by the University of Michigan, have shot up to a level we haven’t seen in 30 years.

So this seems like a good week to do a primer on inflation — history, causes and prospects. Spoiler: Trump’s policies will indeed raise prices, probably substantially, over the near future. But they won’t cause a sustained rise in inflation unless Trump also politicizes the Federal Reserve.

Beyond the paywall:

1\. A brief history of U.S. inflation

2\. Why money isn’t everything

3\. The Biden inflation cycle

4\. Trumpflation?

*A brief history of inflation*

In his new (and fun) book *[How Not to Invest](https://www.amazon.com/dp/1804091197/?bestFormat=true&k=how%20not%20to%20invest%20ritholtz&ref_=nb_sb_ss_w_scx-ent-pd-bk-d_de_k0_1_6&crid=37AMT8ST9YOUI&sprefix=rithol)* Barry Ritholtz devotes a couple of pages to the now-infamous 2022 prediction by Larry Summers that getting inflation down would require a sustained period of very high unemployment — “two years of 7.5% unemployment or five years of 6% unemployment.” Barry attributes that bad call to generational bias: “Summers came of age as an economist in the 1970s,” which predisposed him to see stagflation lurking under the bed. I resent that a bit — Larry and I are almost exactly the same age, and I was emphatic in [declaring](https://www.nytimes.com/2022/08/12/opinion/inflation-1980s-recession-biden.html) that we were *not* headed for a replay of 70s-style stagflation.

I’ll come back to that debate later. For now, my point is that many people — not just economists of a certain age — automatically associate “inflation” with “the 1970s”, a period of sustained high inflation that was only brought under control with a severe recession and years of high unemployment. But there have in fact been many other inflationary episodes even in U.S. history, not to mention the histories of other nations. And these episodes don’t all look the same! As a result, trying to apply the lessons of history when analyzing inflation is tricky. Which history is relevant?

In July 2021, as the most recent inflation surge was building, three Biden administration economists — Cecilia Rouse, Jeffery Zhang, and Ernie Tedeschi — released a [paper](https://bidenwhitehouse.archives.gov/cea/written-materials/2021/07/06/historical-parallels-to-todays-inflationary-episode/) describing U.S. inflationary episodes, defined as periods when inflation went above 5 percent, since World War II. They identified six such episodes:

s_!5CxX!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F7089294d-4f3a-4079-801c-98665a171b94_1264x730.png)

The inflation of the 1970s was the longest such episode, and the one that people remember. But Biden’s economists argued that it was a poor model for what was happening in 2021, which they attributed largely to supply disruptions as the economy emerged from the Covid pandemic.

A better parallel, they argued, was the inflation surge after World War II, as America struggled with the adjustment back to a peacetime economy. As they noted, that inflation surge was intense but transitory: as the economy adjusted, inflation quickly faded away without a prolonged period of high unemployment.

A few economists, notably Joseph Gagnon at the Peterson Institute for International Economics, argued that there were also parallels with the Korean War inflation, which was similarly intense but transitory.

These analyses have aged well, while comparisons to the 70s have not. Inflation went higher and stayed elevated longer than those Biden economists expected, and we still aren’t fully back to prepandemic inflation. Nonetheless, if we extend the inflation timeline to the present, the Biden-era surge looks a lot more like the postwar surge than the 70s. Inflation shot up only temporarily, then faded away without a recession or high unemployment:

As an aside, some prominent economists who got disinflation wrong, predicting severe costs, have not dealt gracefully with the fact that they made a bad call (which happens to everyone!) But that’s not a fight worth getting into, at least in this post.

The important point is to beware of one-size-fits-all approaches to inflation. History can tell us a lot about the causes of inflation and its likely future path; in retrospect, that Rouse/Zhang/Tedeschi paper was a shining example of using history to shed light on current events. But one thing history also tells us is that not all inflations are the same.

Unfortunately, that’s a lesson many people in positions of power have chosen not to learn.

*Money isn’t everything*

> Explanations exist; they have existed for all time; there is always a well-known solution to every human problem — neat, plausible, and wrong**.**

[H.L. Mencken](https://quoteinvestigator.com/2016/07/17/solution/), 1920

Mencken wasn’t talking about inflation, but his famous (often misquoted) remark definitely applies to the subject.

Specifically, the “well-known solution” to the problem of inflation is that inflation is caused by printing too much money — full stop.

Even Milton Friedman knew better than that, although to find that out you need to read his academic papers rather than his writing for the general public. But out there in the world of political advocacy, the simple notion that Money supply => Price level all too often rules.

Here, for example, is Scott Bessent, the Treasury secretary, “explaining” why Trump’s tariffs [wouldn’t raise prices](https://www.cnn.com/2024/11/25/business/ceos-react-bessent-trump-treasury-pick/index.html):

> Tariffs can’t be inflationary because if the price of one thing goes up, unless you give people more money, then they have less money to spend on the other thing, so there is no inflation. The inflation comes through either increasing the money supply or increasing the government spending, and that’s what happened under Biden.

Hoo boy. He said this, by the way, at a time when much of Wall Street was celebrating his selection, believing that he would be a sensible, moderating influence. This quote alone should have warned everyone that he would be no such thing.

What’s wrong with Bessent’s remarks? One minor problem is, what does he mean by “the money supply”? Modern economies don’t rely much on physical currency, so we clearly don’t mean the number of pieces of green paper bearing portraits of dead presidents. Clearly we need to include various kinds of bank deposits, but what about money market funds? What about repo, the overnight lending many corporations use as a way to park their funds and earn slightly higher returns than banks offer? The truth is that at this point there isn’t a consensus on how to measure the money supply, which is OK, because the Federal Reserve stopped paying much attention to these measures decades ago.

The bigger problem with Bessent’s remarks is the blithe assertion that if tariffs raise the prices of imports, other prices will just fall to compensate. The truth is that in a modern economy most companies are reluctant to cut prices, even when demand for their products is weak.

They’re especially reluctant to [cut wages](https://www.hup.harvard.edu/books/9780674009431), which are a large part of their costs, even when unemployment is high and wage cuts wouldn’t impair their ability to retain or attract workers, because they fear the effects on worker morale. They’re also, for more complex reasons, reluctant to make frequent changes in their own prices. Most companies change prices only at intervals, typically once a year, and prices are often “sticky” because sellers are looking over their shoulders at the prices charged by both competitors and suppliers, and don’t want to get too far out of line.

We got a clear illustration of this stickiness during the euro crisis of the early 2010s, when some southern European countries were forced into harsh austerity policies that produced extremely high unemployment. In Spain, for example, unemployment rose to Great Depression levels. This ended the inflation Spain had been experiencing before the crisis, but the overall level of prices flatlined rather than falling:

s_!dzCS!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fc392f9af-3ff9-4819-a350-8c7c27e6980c_800x450.png)

Give this reality, Bessent’s assertion that tariffs will simply be offset by price declines elsewhere is pure fantasy.

Now, monetary stories about inflation work in extreme cases. When governments print money to cover their bills, and the money supply (by any measure) is rising at hundreds or thousands of percent each year, this will indeed cause inflation.

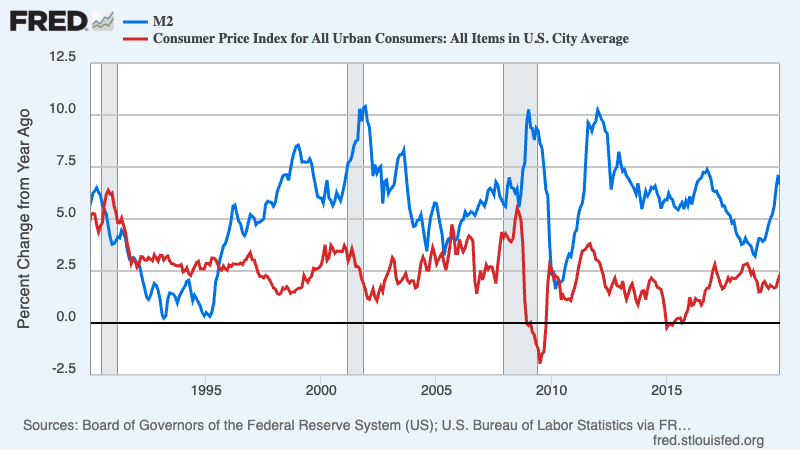

But such experiences hold few lessons for the United States, which doesn’t rely on the printing press to cover its bills and considers 5 percent inflation high. As I mentioned at the beginning of this post, U.S. inflation between 1990 and 2019 was low enough that people didn’t think about it much. As it turns out, there was a lot of variation in the money supply over that period — but these fluctuations had no visible effect on inflation:

None of this means that the Federal Reserve, which can effectively control short-term interest rates by adding to or subtracting from bank reserves, is irrelevant. It can fight inflation by raising interest rates, sending the economy into a recession. It can feed inflation by keeping rates too low and allowing the economy to overheat. But the idea that inflation is only about the money supply is all wrong and completely unhelpful in understanding recent inflation.

The Biden inflation cycle

President Biden enacted the American Rescue Plan soon after taking office. It was big — \(1.9 trillion, which is a lot even in an economy as big as ours. And some economists, notably Larry Summers, warned that it would overstimulate the economy and be highly inflationary. Other economists, myself included, downplayed the risks. Large parts of the bill, like aid to state and local governments, wouldn’t do much to stimulate the economy right away; that money would be spent gradually. Also, historical experience seemed to show that even if the economy became overheated, this would lead to a relatively modest and temporary rise in inflation. Obviously we were wrong to be complacent, and I have [admitted that](https://www.nytimes.com/2022/07/21/opinion/paul-krugman-inflation.html). Inflation quickly shot up to rates not seen in four decades: s_!keXV!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fd60b4699-99e5-4501-a4cb-62b14cf9d6f1_800x450.png)

Alert readers will notice that this chart doesn’t use the ordinary Consumer Price Index. It uses the Harmonized Index of Consumer Prices, which is how European statistical agencies measure inflation, but is also available for the United States. I use that measure to facilitate international comparisons. But for 2021-22, it doesn’t matter what measure you use: inflation did, in fact, soar. Why?

It would be foolish to deny that the Biden stimulus played some role in pumping up demand and hence feeding inflation. But there were other things happening too, largely disruptions associated with Covid and its aftermath. Consumer spending revived after the initial shock of the pandemic, but people spent their money differently from before. Notably, they became reluctant to consume services, which often involve in-person contact and the risk of infection. Instead, they bought physical stuff: kitchen equipment instead of restaurant meals, exercise equipment instead of going to the gym, and more.

And it turned out that supply chains — the infrastructure that gets stuff to consumers — didn’t have the capacity to handle the sudden rise in demand for physical goods. For example, there was a period when container ships were steaming back and forth off the coast of California, waiting for a chance to unload.

The New York Fed calculates an index of supply chain pressures, which spiked briefly during the worst of the pandemic (remember the toilet paper shortage?), subsided, then surged in 2021-22 — a surge that correlates closely with the surge in inflation:

Global Supply Chain Pressure. Source: Federal Reserve Bank of New York.

The good news was that the kinks in supply chains mostly got worked out in the second half of 2022, and inflation came down soon after, falling almost as fast as it had risen.

One additional piece of evidence that supply disruptions played a key role in inflation is that the rise and fall of inflation was a global phenomenon. Europe didn’t have a Biden stimulus, but European inflation nonetheless followed more or less the same trajectory as U.S. inflation, just with a lag.

In the end, inflation followed the script laid out by Rouse et al in mid-2021: a transitory rise in inflation caused by Covid-related disruptions, fading out as the economy adjusted.

Why, then, did Summers and others make such dire pronouncements in 2022, predicting that disinflation would require years of mass unemployment?

Well, remember what I said about how companies don’t revise prices too often and look over their shoulders at competitors and suppliers each time they do adjust their prices.

One consequence of this staggered price-setting, pointed out by [Edmund Phelps](https://www.nobelprize.org/prizes/economic-sciences/2006/popular-information/) in the late 1960s, is that inflation can become “entrenched” in the economy. If high inflation has persisted for some length of time, it will tend to persist. Why? Because every time a company changes its prices, it will usually mark them up both to catch up with inflation that has happened since its last price revision and to get ahead of the inflation it expects to happen before its next revision. So inflation becomes self-perpetuating, which is what happened in the 1970s.

Breaking that cycle in the 1980s required putting the economy through the wringer, with years of very high unemployment. Summers and other inflation pessimists like [Jason Furman](https://www.hks.harvard.edu/centers/mrcbg/programs/growthpolicy/inflation-and-scariest-economics-paper-2022-jason-furman) argued that reversing the inflation surge of 2021-22 would require similar pain. But they were wrong.

I have to admit that I found their position baffling, because it seemed obvious that inflation in 2022 *wasn’t* entrenched the way it had been in 1980. In particular, business expectations of future inflation had remained subdued despite the 2021-22 price surge. Here, for example, is expected inflation from the quarterly Survey of Professional Forecasters conducted by the Philadelphia Fed. (It’s actually the expected change in yet another inflation measure, the GDP deflator, but never mind.):

s_!Ggon!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F41a35b67-40ba-4dd0-add8-d6213cd5cae4_1204x648.png)

Source: Survey of Professional Forecasters

It’s true that forecasters don’t set business prices, but the Survey probably gives us a pretty good sense of the general consensus in the business world. And even when recent U.S. inflation peaked, there was nothing like the circa 1980 belief that inflation would remain very high for years, a belief that had to be broken with a severe recession.

Indeed, high inflation didn’t persist; at the end of 2024 inflation was at most a fraction of a percentage point above the Fed’s target. But the public was still angry over high prices, and a significant number of voters believed Trump when he said he would bring grocery prices down on Day One of his presidency.

It was an absurd promise, and the public seems to have quite suddenly realized that almost everything Trump is doing on the economic front will increase, not reduce, inflation. But how bad will Trumpflation get?

Trumpflation

During the 2024 presidential campaign Donald Trump clearly stated his intention to pursue policies that the great majority of economists believed would stoke inflation: high tariffs, widespread deportation of immigrant workers, and erosion of Federal Reserve independence.

Yet most voters don’t seem to have understood the inflationary impacts of Trump’s policy ideas, while businesses and investors didn’t take Trump’s promises seriously. They expected him to behave the way he did in his first term, pursuing some unorthodox policies at the margin but mostly just cutting taxes and eliminating regulation.

At this point, however, it’s clear that Trump’s old restraint is gone.

Trade War 2.0 is already much bigger than the limited trade war of 2017-18. We don’t know where things will end up, but at this point it will be really surprising if we don’t end up with 25 percent or more tariffs on most of our major trading partners. Deportations haven’t really ramped up yet, but reports say that Trump is frustrated that they aren’t happening faster, and it’s a good bet that we’ll be seeing large-scale arrests and possibly the creation of major detention facilities soon. I’ll get to the Fed later.

How big will the inflation impact be? Imports of goods are about 11 percent of GDP, so a 25 percent tariff would, other things equal, raise prices by about 0.25*11=2.75 percent. A crackdown on undocumented workers — which we can already see would probably sweep up many legal immigrants too — would wreak havoc on agriculture, meat processing, construction and more, although it’s hard to put a number on this until we have a better idea of just how far the crackdown will go.

All in all, however, it seems likely that we’re looking at a self-imposed inflation shock comparable to or exceeding the size of the supply-chain disruptions of 2021-22.

This inflation shock might be mitigated if Trump’s tariffs lead to a stronger dollar. The logic here is that if tariffs reduce our spending on imports, that reduces the number of dollars we’re supplying to the world, which should cause the dollar to rise against other currencies like the euro, which in turn would make other countries’ exports to the United States cheaper in dollars.

But it’s not a given that the dollar will strengthen. For one thing, many of Trump’s tariffs will raise production costs, hurting exports and making it harder to replace imports despite tariff protection. For another, other countries will retaliate. And I’m thinking a bit about the foreign trade consequences of being ruled by madmen — more about that in another post.

Still, comparing the Trump shock to Covid-related supply disruptions has an upside. Remember, those disruptions caused a one-time bump in prices, not a sustained rise in inflation. Won’t the same be true of the impact of tariffs and deportations?

As someone whose political leanings aren’t a mystery, I’d like to say no, that Trumpflation will be much worse and more sustained than anything we experienced under Biden. But that’s a hard case to make. Given what we know now, I’d expect to see a year or two of nasty inflation, but not a return to 70s-style stagflation.

That is, that’s what to expect if Trump keeps his hands off monetary policy. If he doesn’t — if, for example, he’s frustrated by the persistence of U.S. trade deficits and forces the Fed to cut rates to weaken the dollar — then all bets are off.

Are we winning yet?

- Reference: https://paulkrugman.substack.com/p/inflation

Write a comment