Money Isn’t Everything

WONK ALERT: TODAY’S PRIMER WILL BE (EVEN?) MORE ECONOMISTIC THAN USUAL. YOU HAVE BEEN WARNED

This week’s primer will be a bit self-indulgent. In the weeks ahead I expect to be writing about demography, immigration, Social Security, health care costs, energy and more. But this week I’ll engage in one of my running pastimes, chasing down zombie economic ideas — ideas that should have been killed by evidence, but keep shambling along, eating people’s brains.

Specifically, I want to focus on a case of bad economic theory that I have been seeing a lot lately: The revival of “vulgar monetarism” — the idea that inflation is entirely a matter of the money supply.

Here’s an example of what I mean. In December Scott Bessent, now the Treasury secretary, dismissed the idea that the Trump tariffs would be inflationary:

Tariffs can’t be inflationary, because if the price of one thing goes up, unless you give people more money, then they have less money to spend on the other thing, so there is no inflation. … Inflation comes through either increasing the money supply or increasing the government spending, and that’s what happened under Biden.

This is all wrong, and the wrongness matters. It matters for understanding the impact of tariffs. It also matters for how we interpret the inflation spike of 2021-23, which is central to Bessent and Trump’s attack on the Fed’s independence.

According to Bessent’s logic, the Covid-induced supply-chain disruptions— remember all those freighters steaming back and forth, because they couldn’t land their cargo? — weren’t the source of the 2021-23 inflation spike. Instead, he claims, all the blame rests on the Federal Reserve for printing too much money. This Bessent claims, in his ongoing smear campaign against the Fed, is a pretext for destroying away the Fed’s independence.

So let’s go zombie hunting. Beyond the paywall I will discuss the following:

1. The monetary explanation of inflation – when it’s right and when it’s wrong

2. The source of Biden-era inflation

3. What are sticky prices and why they matter in understanding inflation

4. Tariffs and inflation

Money and inflation

Somewhere — I haven’t tracked down the reference — James Tobin offered a nuanced critique of Milton Friedman’s work on monetary economics. Friedman, Tobin said, had produced a great deal of solid, important evidence refuting the claim that the money supply is not a factor in causing inflation. But, Tobin suggested, Friedman all too often elided the difference between “money does too matter” and “only money matters.” Or to cite a frequently quoted Friedman line that proves Tobin’s point, “Inflation is always and everywhere a monetary phenomenon.”

I understand the appeal of a money-only view of inflation. It’s not simply a matter of ideology, although that too. It’s also an illustration of H.L. Mencken’s dictum: “For every complex problem there is an answer that is clear, simple and wrong.”

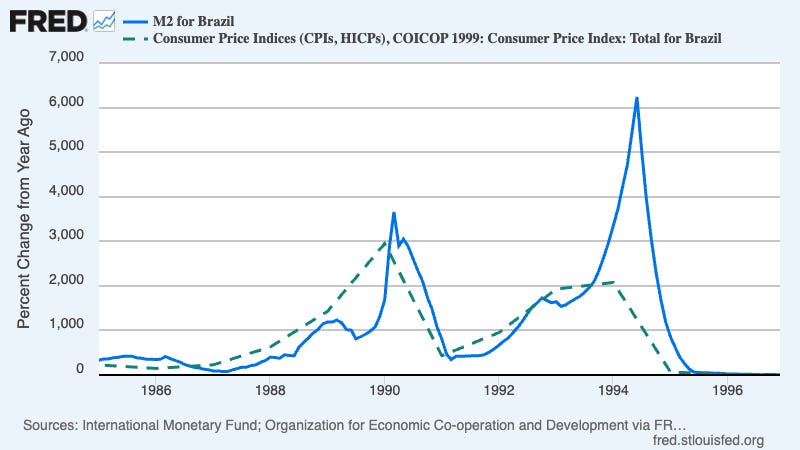

Now, I don’t know any serious economist who would dispute the fact that large increases in a nation’s money supply — usually defined as currency in circulation plus bank deposits — will normally be inflationary. For example, the chart below illustrates Brazil’s experience during the late 1980s and early 1990s, in which runaway growth in the money supply (the solid blue line) drove runaway inflation (the dashed green line):

in the economy led to a large rise in the money supply (the solid blue line), yet this didn’t lead to a large rise in consumer prices (the dashed green line): s_!MGTQ!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F9289e78b-8d87-40c7-afe4-d646cd0dff79_800x450.png](https://substackcdn.com/image/fetch/\(s_!o1T4!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F0aecde59-c3e6-490e-a644-70ce60205830_800x450.png)

But in a depressed economy, large increases in the money supply often *aren’t* inflationary. An example is illustrated in the chart below. In the aftermath of the 2008 financial crisis, the Fed’s efforts to mitigate the [sustained slump](https://paulkrugman.substack.com/p/scott-bessent-sleazy-smearer) in the economy led to a large rise in the money supply (the solid blue line), yet this didn’t lead to a large rise in consumer prices (the dashed green line):

s_!MGTQ!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F9289e78b-8d87-40c7-afe4-d646cd0dff79_800x450.png){kind=link}

As I noted in my previous post about Bessent, many on the right predicted that the Fed’s post-financial-crisis monetary expansion via “quantitative easing” would be inflationary. But, in fact it wasn’t. The economy remained depressed, with inflation hovering below 2 percent and interest rates close to zero.

Instead, Bessent claims that the quantitative easing of the financial crisis years caused the inflation critics wrongly predicted. Yes, there was also a large expansion in the money supply during Covid. But since the economy was again depressed due to lockdown, with interest rates again hovering close to zero, there is no evidence that the Covid-era increase in the money supply was the cause of inflation.

The larger point, consistent with Tobin’s critique of Friedman, is that increases in money supply are not the sole source of inflation. In other words, there can be bursts of inflation that are caused by factors other than monetary expansion. For example, the inflation spikes in 1990 and again in 2008 were caused by spikes in world oil prices:

s_!uKyp!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa8c34801-038e-456a-a67f-91585da74e0b_1292x806.jpeg](https://substackcdn.com/image/fetch/\(s_!b-AD!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fc1a9bb8d-a103-45db-ab13-8267e194af0f_1262x710.jpeg)

Source: Council of Economic Advisers

In addition to accounting for much of the price of gasoline, oil is a major input in production. So oil-price shocks to inflation are an example of how disruptions in the supply of goods and services in the economy can have major inflationary impacts. Now let’s examine another example: covid-era inflation caused by supply-chain disruptions.

*Covid-era supply-chain inflation*

For several months during 2020, large parts of the U.S. economy were locked down in order to limit the spread of Covid. While some of the lockdown measures were mandatory, much of the paralysis of the economy reflected individual choices: wary of infection, many Americans shunned regular activities such as in-person shopping, restaurant dining and dentist appointments.

In 2021, as covid vaccines became available and the pandemic subsided, consumer spending quickly recovered. However, consumers spent their money *differently* compared to pre-Covid. They still avoided in-person activities, often purchasing physical substitutes instead. For example, people bought kitchen equipment and home exercise equipment, preferring to eat and exercise at home rather than going to restaurants and gyms.

Overall, consumption shifted away from services toward goods. Yet we didn’t have the physical infrastructure to meet the expanded demand for physical goods. Notably, there was insufficient capacity in the container ports through which imported goods arrive to handle the flood of goods. There was even a global shortage of shipping containers.

The graph below shows one symptom of the pressure on supply chains, a surge in international shipping costs that only began to subside in 2022:

s_!uKyp!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa8c34801-038e-456a-a67f-91585da74e0b_1292x806.jpeg){kind=link}

Predictably, snarled supply chains affected goods much more than services. Normally, prices of goods rise more slowly than prices of services, because technological advances have historically been faster for goods than services – think electronics versus haircuts. But during the post-Covid disruptions, goods prices temporarily rose much more rapidly than service prices due to the supply chain problems. This is illustrated by the chart below, where the solid blue line tracks the prices of goods and the dashed green line tracks the prices of services:

For our purposes, here’s the important question: How much of the temporary rise in overall inflation can be attributed to the supply chain disruption rather than from monetary expansion? If you want a detailed, careful analysis, I’d recommend this [piece](https://bidenwhitehouse.archives.gov/cea/written-materials/2024/07/30/inflations-almost-roundtrip-what-happened-how-people-experienced-it-and-what-have-we-learned/) by Jared Bernstein. But let me offer a quick-and-dirty, back of the envelope analysis. If you look at the chart above, you see that goods price inflation rose about 10 points, from zero before Covid to 10 at its peak. Service price inflation rose only about a quarter as much, from around 2.5 percent to 5 percent.

Now, services are a larger component of consumer spending than goods — roughly two-thirds, versus one third for goods. But this still says that about two-thirds of the rise in overall inflation can be attributed to goods prices, which in turn were surging largely because of supply-chain disruptions.

Moreover, it’s reasonable to attribute more that two-thirds of inflation to supply chain problems because service providers must also purchase a lot of goods in delivering services to consumers. For example, doctors and hospitals have to buy pharmaceuticals, medical equipment, and more. So supply-chain disruptions also contributed to service inflation during this period.

One additional piece of evidence that supply-chain issues, and not Fed monetary expansion, were the major driver of the 2021-2023 inflation spike in 2021-23: the fact that supply-chain disruptions were a global phenomenon and inflation rates were extraordinarily similar around the world. Now, to make a valid comparison of inflation rates in various countries, you have to be careful to compare apples to apples — or, as one Council of Economic Advisers report put it, [apples to Äpfel](https://bidenwhitehouse.archives.gov/briefing-room/statements-releases/2023/06/27/cea-apples-to-apfel-recent-inflation-trends-in-the-g7/). The U.S. consumer price index is constructed quite differently from inflation measures used in other countries. However, the Bureau of Labor Statistics estimates what the U.S. inflation rate would be if we used a measure similar to the European standard~.~ What this measure (the solid blue line below) shows when compared to the European measure of inflation (dashed green line below) is that inflation spiked on both sides of the Atlantic. Furthermore, the spikes were remarkably similar even though the United States did considerably more monetary and fiscal stimulus than Europe:

s_!DF9z!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F169e5b69-131c-47d1-8e1c-05c8dbb67ffe_800x450.png)

So the evidence strongly suggests that the inflation surge of 2021-2023 was not a monetary phenomenon; rather, it was largely caused by post-Covid supply disruptions.

But wait — does the evidence really say that? I often encounter arguments to the effect that supply problems only caused inflation because the Fed allowed that to happen, that inflation could have been avoided if the Fed had kept a lid on the money supply. So let me explain that argument, and what’s wrong with it.

The importance of price stickiness

In the aftermath of Covid, Americans wanted to consume more physical goods and fewer services than before. But since we didn’t have the infrastructure to deliver all those additional goods, prices of goods rose in comparison to the price of services.

But would it have been possible for the average level of prices to stay the same? You could imagine a scenario in which the prices of goods went up but the prices of services fell, so that the average level of prices remained the same.

That’s basically the claim that Scott Bessent made about tariffs, quoted at the beginning of this post. Sure, he says, tariffs will raise the prices of imported goods, but if you don’t increase the money supply, prices of goods and services that aren’t subject to tariffs will fall, so the average level of prices won’t change — no inflation.

Some readers will note that the Trump administration also insists that tariffs won’t raise import prices, that the cost of the tariffs will be borne entirely by foreigners. But that’s another bad argument, which I’ll ignore in this post.

So what’s wrong with Bessent’s argument ? The answer is that his argument requires that the prices of non-imported goods fall. In fact, widespread price declines are actually quite rare, and generally happen only in the face of widespread distress.

Why? First, most producers can’t cut their prices, at least significantly, unless they can get their workers to accept significant wage cuts. And wages very rarely fall, except in the face of very high unemployment. For example, almost no countries saw significant wage declines even in the aftermath of the 2008 financial crisis. The exception was Greece, where the unemployment rate reached 28 percent.

The economist Truman Bewley explained “downward nominal wage rigidity” in a classic book, “Why Wages Don’t Fall During a Recession.” Bewley did something rare among economists: He actually went and talked to businesspeople. He asked why they didn’t cut wages even when there was high unemployment, hence plenty of people willing to work even for lower wages. The answer he got was that any business cutting wages would anger and demoralize its work force, and the cost of reduced productivity and increased conflict would outweigh the direct cost savings.

The fact that companies normally can’t and won’t cut wages is enough, by itself, to explain why refusing to increase the money supply isn’t enough to prevent inflation caused by supply disruptions or tariffs. But companies are also reluctant in general to cut prices (except for temporary sales), over and above the problem of sticky wages. Why? One important reason is probably that they don’t want to make price cuts they’ll eventually have to reverse, because they know that they will anger their customers when they hike prices again.

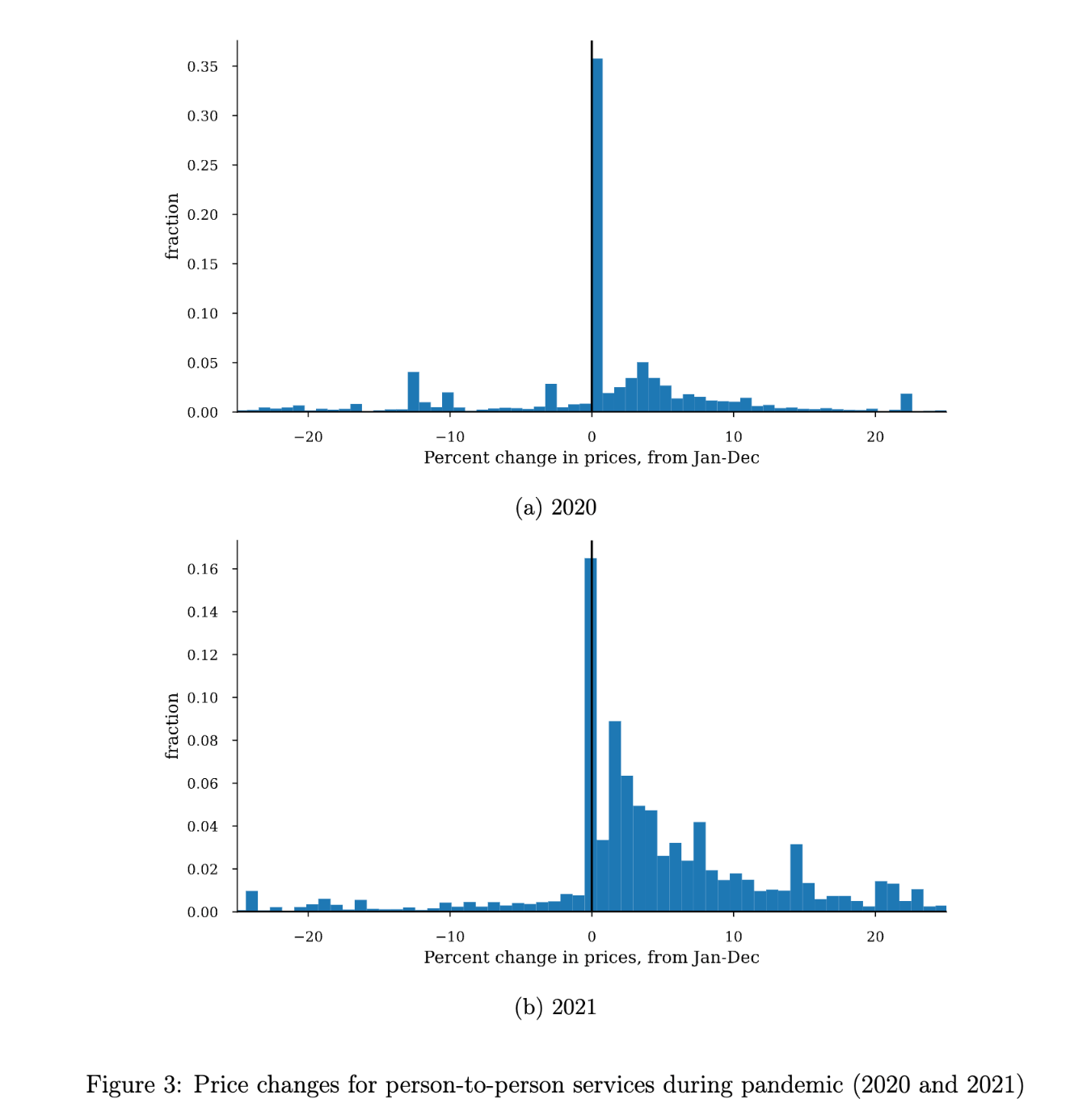

There’s solid evidence for downward rigidity in prices. For example, Bonam and Hobijn have data from prices of British firms selling person-to-person services during the pandemic. Like their U.S. counterparts, these firms saw a large decline in business during that period. The bars in the charts below show the fraction of firms making price changes of different sizes in 2020 and 2021:

{kind=link}

Source: Bonam and Hobijn

In both years there was a big spike at zero — that is, a large fraction of firms neither raised nor reduced prices. This was almost certainly because these firms were facing very weak demand, so they couldn’t raise prices, but didn’t want to cut prices either.

As I noted, we only see prices fall in the midst of a depression. So when someone says that increased prices due to supply constraints or tariffs need not result in inflation, because those price increases will be offset by price cuts elsewhere, what they are really arguing is that the Fed should engineer a depression because that is only way to achieve price cuts. Blaming the Fed for inflation in 2021-23 is, in effect, saying that the Fed should have been willing to accept a depression rather than allow a temporary rise in inflation due to Covid-induced supply disruptions.

And what about tariffs?

Tariffs and inflation

The average U.S. tariff rate has jumped from less than 3 percent at the beginning of this year to more than 17 percent now. There is no evidence that foreign exporters have cut prices to offset these taxes, hence the burden falls on Americans. At this point, U.S. businesses are temporarily absorbing much of the cost and only part of the tariffs have been passed through to consumers. But that isn’t sustainable and a number of companies, Walmart included, have said that they will begin passing on the cost of the tariffs to consumers.

As a result, the prices of imported goods to consumers will rise. And contrary to what Bessent may say, these price increases won’t be offset by declines in the prices of domestic goods. That would only happen if America experienced a depression, which even pessimists don’t expect.

Contrary to Bessent’s assertion, then, tariffs will cause inflation. And the money supply will have nothing to do with it.

Write a comment