The Economics of Stagflation, Part II

In last week’s primer I wrote about what stagflation is, the logic behind it, and its history. Here’s a brief list of what I covered:

· Stagflation is a combination of inflation and high unemployment

· What it means for inflation to become entrenched in the economy: companies and workers raise their prices because they expect everyone else to do the same.

· Taming the inflation of the 1970s required extreme measures by the Federal Reserve, resulting in a severe period of stagflation in the US during 1979-1984, because inflation had become entrenched in the economy

· In contrast, taming the post-Covid inflation of 2022 to 2024 did not require the same harsh medicine because inflation had not become entrenched in the economy. As a result, the Federal Reserve was able to bring inflation down without inflicting high unemployment on the economy.

Today I’ll look forward. Stagflation is very much on people’s minds again, for good reason. The Trump administration’s tariff and deportation policies are creating a significant inflationary shock. They’re also imposing a significant drag on economic growth. Today, it’s likely that the United States would be heading into a recession under the weight of higher prices and slower growth if the economy weren’t being supported by a huge boom in AI-related investment. And this danger remains: if the AI boom goes bust, the odds are high that the US economy will be plunged into a recession.

In talking about stagflation, it’s important to acknowledge that its effects can range from run-of-the mill bad to devastating. For example, in the early 1990s, there was a burst of inflation and an extended period of elevated unemployment. It was bad — but not that bad. That is, there was a mild recession, not a deep and devastating one. But there are also episodes like 1979–1984 (which I covered at length in last week’s primer). In that episode, it took a severe and lengthy recession — many years of high unemployment — for the Federal Reserve to bring inflation under control. Last, as we experienced in the post-Covid period, there can be times when stagflation can be avoided altogether.

What accounts for the difference? That is, what determines if a period of inflation will result in a devastating recession rather than a merely mild recession, or perhaps no recession at all? The answer, as I wrote in last week’s primer, is due to whether inflation or not has become entrenched in the economy. When it has, the Federal Reserve has to send the economy into a severe recession by raising interest rates substantially to purge the price spiral from of the economy. If inflation hasn’t become entrenched, the Federal Reserve can tame inflation without needing to cause high unemployment.

Which scenario will it be this time? I don’t know. The Federal Reserve doesn’t know. Trump administration officials definitely don’t know. But we can talk about the factors affecting how it goes — and what policies might make it better or worse.

Beyond the paywall I’ll discuss the following:

1. The Trump shock and how it’s playing out

2. How will we know if inflation is becoming entrenched?

I’ll reserve discussion of policy — and the crucial role of the Fed’s credibility — for yet another stagflation primer, next week.

The Trump shock

In terms of economic policy, Trump’s first term in office, pre-Covid, was fairly normal — what we might call standard-issue Republicanism. He pushed through a tax cut for corporations and the wealthy similar in size, as a share of the economy, to the tax cuts under George W. Bush. He imposed some tariffs, but they were mainly aimed at China and limited in size. The overall shape of U.S. economic policy at the start of the pandemic wasn’t very different from what it had been when he took office. And the emergency measures taken during the pandemic were huge but had wide bipartisan support.

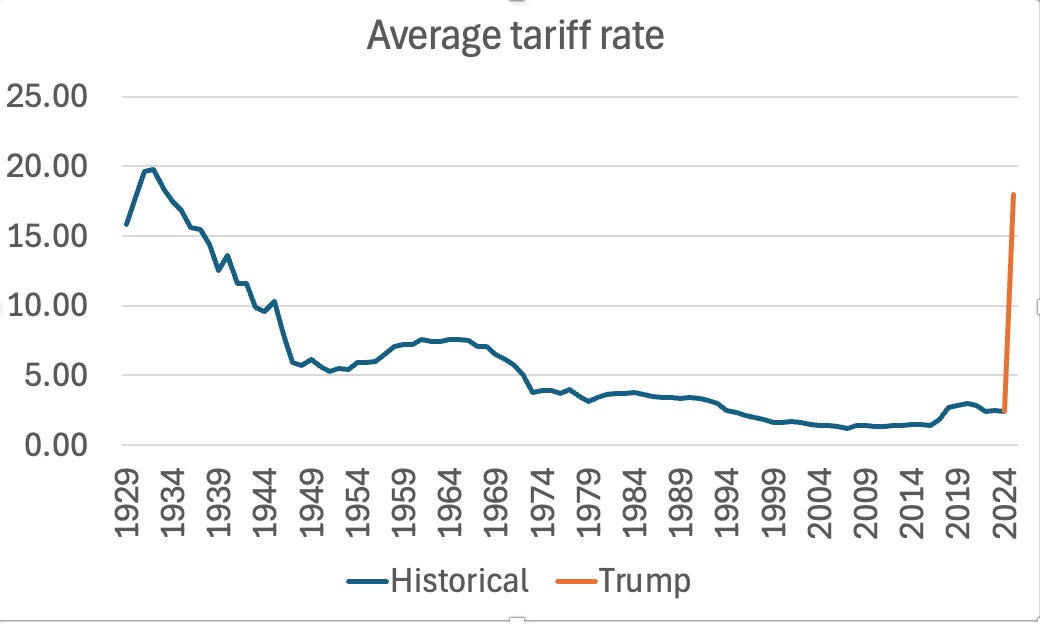

Trump II has been a completely different story. Average tariffs have shot up from around 2 to around 18 percent, reversing 90 years of U.S. trade policy. ICE is now arresting 1500 or more people a day, and the number of foreign-born workers, which grew rapidly in recent years, is almost surely set for a substantial decline. Without workers to pick fruit and vegetables, clean hotel rooms and construct buildings, the prices for many goods and services will definitely go up — if the goods and services are available at all.

Chart 1 Source: Yale Budget Lab

These drastic policy changes, then, are clearly inflationary. They will also probably cause an economic slowdown, although this is less certain. If they do both — or if the economy slows down for other reasons — we will be facing stagflation. In fact, stagflation is probably happening as you read this.

Let’s start with inflation. Trump and his supporters have repeatedly insisted that foreigners will absorb the tariffs, that they won’t raise prices to U.S. consumers. How do we know that they’re wrong?

First, to avoid an impact on U.S. consumers, foreign companies selling to America would have to cut the prices they charge on exports to the U.S. by enough to offset the tariffs. The Bureau of Labor Statistics collects data on the prices paid for imports, not including tariffs. Their import price index shot up during the supply-chain disruptions of 2021-22, declined as supply chains got unsnarled, then began rising again. It has *not* declined since the Trump tariffs went into effect, which tells us that foreign exporters aren’t paying the tariffs:

s_!jWpE!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F6942499d-f9fa-4ca0-9998-78380b9fe343_800x450.png)

Chart 2

There’s also preliminary statistical evidence of a significant rise in retail prices of imported goods. This chart shows prices of domestic (blue line) and imported goods (orange line) at major retailers, with Oct. 1, 2024 set equal to 1.

Chart 3 Source: [Tariff Tracker](https://www.pricinglab.org/tariff-tracker/?utm_source=substack&utm_medium=email)

These data show prices of imported goods rising significantly more than those of domestically produced goods. The differential may look small — 2-3 percent. But you should bear in mind that when you buy an imported good at a store — say, a toy made in China — the cost of bringing that good to America, including tariffs, is only a fraction of the price you pay. So even if the full 15-point rise in tariffs were passed on to consumers, we’d expect retail prices to rise by much less than 15 percent.

That said, consumers still haven’t felt the full effect of tariffs, because U.S. businesses — not foreigners — have been absorbing part of the costs, trying to hold on to customers and hoping that Captain Bligh – er, Trump -- will reverse course. But he clearly isn’t and businesses can’t keep absorbing the costs. For example, Walmart says that tariff costs have been rising “[each week](https://www.npr.org/2025/08/21/nx-s1-5509592/walmart-tariff-costs-rising-earnings)” and that it is beginning to raise prices to offset these costs.

I could go on, but it’s quite clear that tariffs are gradually being passed on to consumers, and that there will be ~a~ substantial increase in consumer prices over the next few months.

There are also preliminary indications that deportations are raising some prices, notably farm products largely harvested by immigrant labor. Here’s the monthly rate of growth in the wholesale price of fresh vegetables, which spiked 50 percent in July:

s_!pEt7!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa0cd78bd-42da-490d-b115-87b34eed6912_1324x852.png)

Chart 4 Source: BLS

The bottom line is that there is no reason to question standard economics here: Tariffs are raising prices, and together with deportations will cause a significant inflationary shock, maybe 2 percent or more added to consumer prices over the next year.

What about the “stag” part of stagflation? Tariffs don’t necessarily lead to high unemployment. For example, as you can see from Chart 1, the average U.S. tariff rate was over 15 percent in 1929, but unemployment that year was low.

However, Trump’s tariffs and, increasingly, his deportations clearly are depressing spending because they are creating huge uncertainty. Tariff rates keep changing. Even when the U.S. makes a “deal” with another country, it’s not at all clear what has been agreed — for example, the U.S. and European descriptions of their supposed deal are quite different. And Trump keeps adding new tariffs, but also new exemptions. And some countries like Brazil — which supplies about a third of our coffee, and faces a 50 percent tariff — may never be able to make a deal because Trump has a special animus towards them.

Under these conditions it’s very difficult for businesses to commit to investments: They have no idea what tariff rates will be even a few months from now, let alone over the lifetime of the investment. Deportations add further uncertainty: Will the labor force a company needs be available?

U.S. job creation has, in fact, slowed substantially since 2024. It’s reasonable to believe that we would be heading into a recession right now if the depressing effect of Trump-inflicted policy uncertainty weren’t being offset by the boom in AI-related spending. If AI spending is at least partly a bubble, a sharp slowdown, possibly a full-fledged recession, is likely when that bubble pops.

And there is a third factor that is currently raising inflation: electricity prices. Electricity prices have risen about 7 percent over the past year, mostly due to the higher energy demand arising from data centers that power AI. With the tens of billions that are being poured into AI, it appears unlikely that the demand for more energy will moderate any time soon. Simultaneously, Trump is destroying our best new energy sources: green energy from wind and solar.

So it’s very likely that stagflation is unavoidable. The big question is what kind of stagflation — a relatively mild, temporary episode like the early 1990s, or an extremely painful adjustment like the one at the end of the 1970s.

Will inflation become entrenched?

Saddam Hussein invaded Kuwait in August 1990. The opening of the first Gulf War sent world oil prices soaring. As you can see in Chart 5, higher fuel prices led to a temporary surge in U.S. inflation.

America entered a recession at almost the same time, leading to a substantial rise in unemployment. Oil prices may have contributed to the slump, but the main cause was the collapse of a bubble in commercial real estate.

So America in 1990-91 experienced inflation combined with recession — stagflation. It was a difficult time for the economy, especially because recovery from the recession was sluggish. In November 1992 the economy still felt bad enough that voters defeated the incumbent president, George H.W. Bush and delivered the White House to Bill Clinton.

So the stagflation of the early 1990s was painful. But as the graph below shows, inflation (solid line) came down rapidly, while unemployment (dashed line) was elevated without being catastrophic.

Chart 5

In other words, the early-90s stagflation was nothing like the Great Stagflation of 1979-1984, when both inflation and unemployment remained very high for years:

s_!av-W!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F7cc97d5c-bc3c-46f6-8841-015880b45b83_2030x1060.png)

Chart 6 Source: FRED

In Part I of this primer I explained what made the Great Stagflation so devastating. Years of irresponsible policy in the 1970s had allowed inflation to become entrenched: inflation was self-sustaining because companies were engaged in a game of leapfrog, continually raising prices to catch up with past inflation and get ahead of expected future inflation. So it took years of high unemployment to squeeze inflation back down to tolerable levels.

But that didn’t happen in 1990. Even more impressively, it didn’t happen in 2021-22, when inflation really shot up as a result of Covid-related supply disruptions, then came down without any recession at all. That’s because, as I noted earlier, inflation had not become entrenched in the economy during either of those episodes.

The trillion-dollar question now is whether the Trump shock will, like the post-Covid supply chain shock, have only a transitory effect on inflation, or whether it will cause inflation to become entrenched as it was during the 1970s.

On the one hand, I can make a plausible case that the Trump shock will not result in entrenched inflation. After all, tariffs and deportations will cause only a one-shot rise in prices, not continuing upward pressure. Hence companies may not believe that they need to keep raising their prices to stay even.

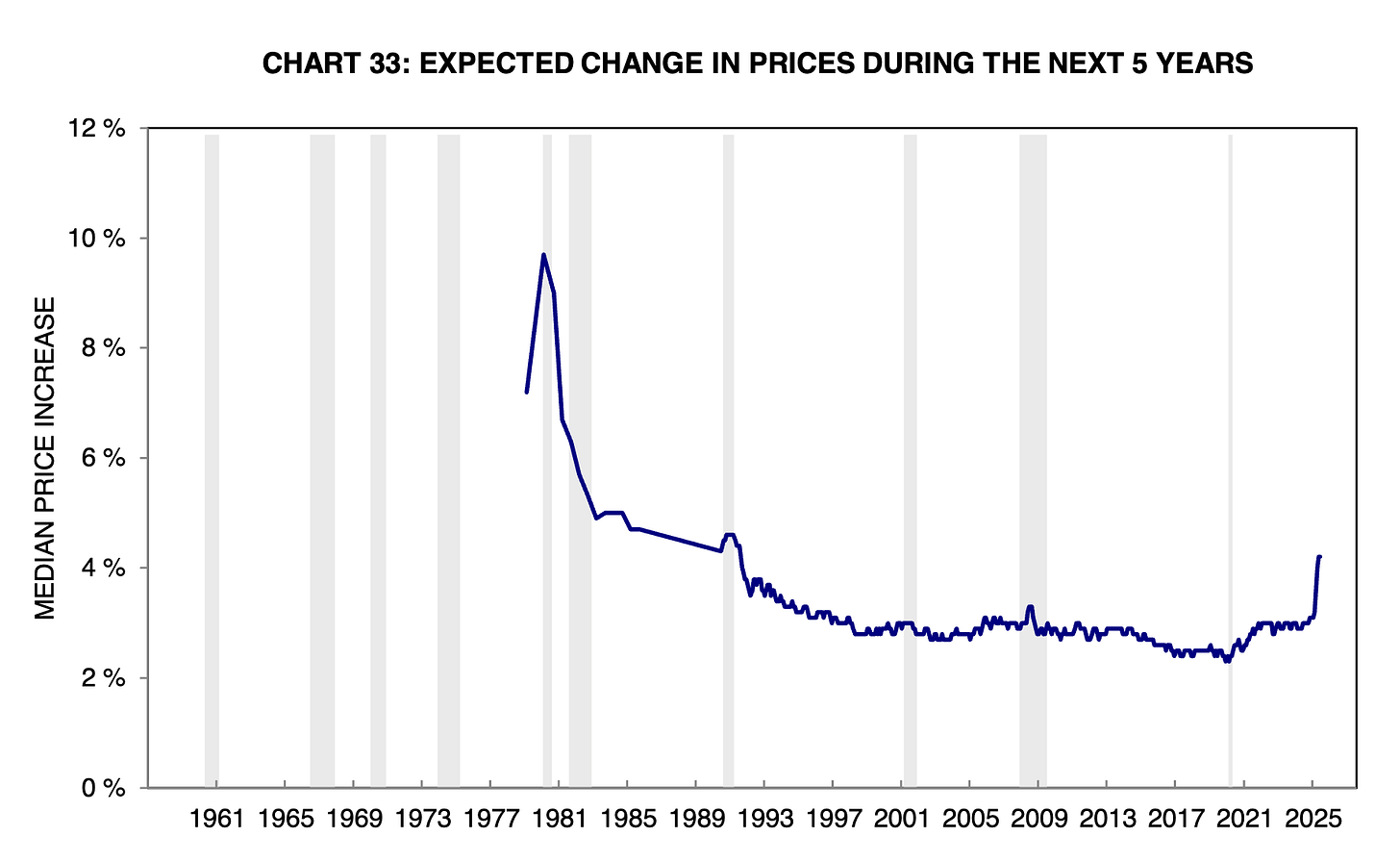

On the other hand, I can also make a reasonable case that the Trump shock will turn into entrenched inflation. One worrisome sign comes from consumer expectations. One reason some of us thought that analogies with the Great Stagflation were misleading back in 2022 was that in 2021-22 long-term inflation expectations, which were very high in 1980, stayed low despite a spike in inflation:

Chart 7 Source: Michigan Consumer Surveys

But this time, as you can see from Chart 7, the Trump shock has already led to a sharp rise in expected inflation.

So what will happen? Even more to the point, what should the Federal Reserve be doing?

Unfortunately, this primer is already long — and we may have some relevant news in the next few days. So that, plus the crucial importance of Fed credibility, will be the subject of next week’s primer. Stay tuned.

Write a comment