A Primer on Financial Crises, Part II

Last week I posted Part I of a primer on financial crises. Although the post was motivated by the wild market action after Donald Trump unveiled his Rose Garden tariffs, it was getting too long, so I promised to address current events today. To be honest, I was also hoping that the situation would become clearer after a week.

It hasn’t. We seem to have stepped back a bit from the ledge, largely because Trump scrapped his original tariff plan and replaced it with something markets perceived — wrongly — as less extreme. But things remain deeply unsettled.

Rather than wait for a resolution that may be a long time coming, however, let me continue the primer by talking about how policy interventions can sometimes act as circuit breakers that help avoid financial crisis. I’ll follow that with an attempt to make sense of where we are now and discuss what the future may hold.

Policy interventions in financial crises

Asset prices sometimes fall. Sometimes they fall spectacularly. One example is the epic NASDAQ decline of the early 2000s, in which investors finally realized that tech profits would never be high enough to justify the sky-high valuations of tech stocks. Should policymakers have intervened? The answer is a resounding “no”: policy intervention can’t and shouldn’t prop up asset valuations that fundamentally don’t make sense. There wasn’t anything the Fed or the Treasury could or should have done to keep stock prices near their 2000 peak.

However, a financial crisis is a different matter. The defining feature of a financial crisis, as opposed to a mere fall in asset prices, is its self-reinforcing nature: People are dumping assets because other people are dumping assets. For example, the market meltdown of 2008, which was the functional equivalent of a bank run, was a financial crisis. When people are dumping assets simply because other people are dumping assets, policymakers can and should intervene to break the vicious cycle — for example, by publicly buying or promising to buy the distressed assets.

Last week I distinguished between two kinds of financial crisis. Liquidity crises, epitomized by bank runs, involve a scramble for cash. Balance sheet crises take place when plunging asset prices force investors to sell, driving prices even lower and inducing more selling. In both cases policy intervention can make all the difference, ending the crisis before too much damage is done.

Liquidity crises have often been contained by central banks — the Federal Reserve and its counterparts abroad — that either lend money to banks and bank-like institutions or buy their assets at full price, thereby assuring depositors that they will be able to get their cash out.

In fact, that was the main role originally envisaged for the Federal Reserve, founded in 1913. Back then financial crises were generally referred to as “panics,” and were countered, if at all, with ad hoc private interventions. But J.P. Morgan isn’t always there when you need him. So the Fed was established largely to lend money to cash-strapped banks during panics, with macroeconomic policy (a term that wouldn’t be invented until 1946) something of an afterthought. And acting as the “lender of last resort” remains one of the Fed’s crucial roles.

Most recently, the United States teetered on the brink of a severe liquidity crisis in March 2020. Investors, shocked by the realization that Covid-19 would massively disrupt the economy, were dumping everything, even Treasuries — U.S. government debt — then regarded as the ultimate safe asset. (Thanks to Trump, that status is now in question.) For a few days financial markets basically stopped functioning.

Then the Federal Reserve rode to the rescue, creating an alphabet soup of new lending programs to back banks, businesses and local governments even as it stepped in to buy hundreds of billions of dollars’ worth of Treasuries. The purpose, as Adam Tooze wrote, was to “extend a huge overdraft facility” to the economy, reassuring frightened investors so that they would stop frantically demanding cash.

The intervention succeeded. By the end of March the Treasury market had returned to normal, and within a few months markets in general were on the upswing.

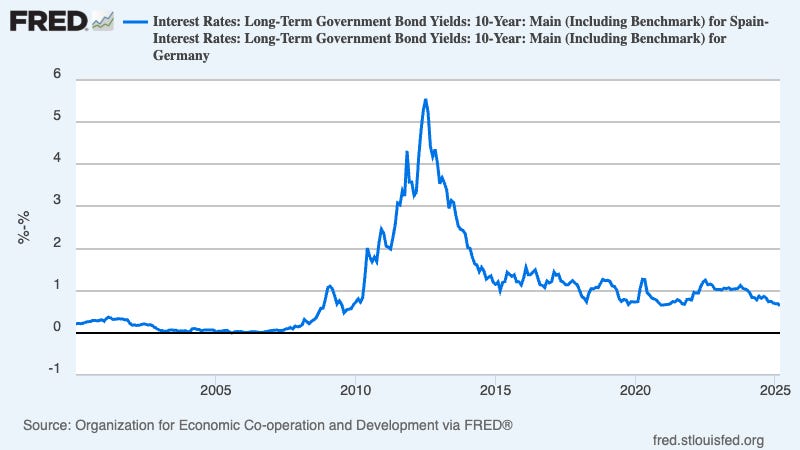

Sometimes the mere promise that the authorities will step in if necessary is enough to end a financial crisis. Last week I mentioned that the euro crisis of the early 2010s, widely viewed as a solvency crisis, turned out to be mainly a liquidity crisis: lenders feared that southern European nations would be forced into default by lack of cash, and the collapse of lending was causing the cash shortage. Mario Draghi’s June 2012 statement that the European Central Bank would do “whatever it takes” was perceived as an assurance that the ECB was ready to buy troubled governments’ bonds, and that perception quickly ended the crisis without the need for any actual bond purchases. Here’s the spread between Spanish and German bonds:

Public intervention can also help contain balance sheet crises. As I explained last week, the [Liz Truss/head of lettuce crisis](https://www.chicagofed.org/publications/chicago-fed-letter/2023/480) of 2022 was largely driven by British pension funds, which were forced by falling prices of gilts — long-term government bonds — to sell gilts themselves, driving prices down further. The Bank of England, the UK’s equivalent of the Fed, eventually intervened, buying large quantities of gilts, and the crisis abated.

As I’ll explain below, Donald Trump’s announcement on April 9 that he was pausing many of the tariff hikes he had proclaimed a week earlier was in a way a kind of crisis-limiting intervention and explains how we (temporarily) stepped back from edge.

But if policy intervention can contain financial crises, why do such crises sometimes spiral out of control? In particular, why did policymakers allow the 2008 crisis to snowball, becoming so severe that it ultimately caused years of high unemployment?

The answer is that, in 2008, key policymakers were initially unwilling to intervene for ideological reasons. Lehman Brothers begged for help as it was caught in a vicious vortex of selling and falling asset prices, yet was allowed to fail. The Wall Street Journal’s editorial page initially praised the decision, [declaring](https://www.wsj.com/articles/SB122144484890334903) that

> the government had to draw a line somewhere or it would have become the financier of first resort for every company hoping to buy a troubled firm. Especially with the Fed discount window now wide open to many more financial institutions, and to many kinds of collateral, Treasury Secretary Hank Paulson's refusal to blink won't get any second guessing from us. If Lehman is able to liquidate without a panic, and especially if its derivative contracts can be safely undone, the benefits would include the reassertion of )

Second, economists normally expect that tariffs, which lead to a reduction in imports and hence a reduced supply of dollars to the foreign exchange market, will cause the dollar to rise against other currencies. Rising U.S. interest rates should also have boosted the dollar. Instead, it fell sharply:

The combination of rising interest rates and a falling currency isn’t normal for the United States. It is, however, something we often see in emerging markets that lose the confidence of international investors, who pull their money out. So one interpretation of market behavior after April 2 is that Trump has managed to convince the world that America is a risky place to put your money.

It’s unprecedented to see what looks like capital flight from the United States. But capital flight from an America now seen as untrustworthy, while shocking, doesn’t meet the definition of a financial crisis. Like the early 2000s decline in the NASDAQ, it’s just markets recognizing reality. But is that the whole story?

I don’t think so. For in addition to rising yields on Treasuries and a falling dollar, we’ve also seen interest rates on relatively risky or thinly traded assets, like [high-yield corporate bonds](https://fred.stlouisfed.org/graph/?g=1IkHT), shoot up. I was especially struck by the fact that interest rates on bonds that are protected against inflation — bonds that are much less widely traded than ordinary bonds — rose so much that the spread between these bonds and regular bonds, often seen as a market forecast of inflation, went down:

s_!S72R!,w_1456,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa566708c-35ca-41fa-9dec-1241f1622ed7_800x450.png)

This was peculiar, because the giant rise in tariffs will surely lead to higher, not lower inflation. But that spread plunged during the 2008 crisis and again in 2020, so it suggested that we may be in the early stages of another financial crisis.

If we are looking at an incipient financial crisis, what’s the mechanism? As best I can tell, we’re looking at a potential balance sheet crisis focused on hedge funds, which own large quantities of risky assets. Like Lehman in 2008, these funds are highly leveraged — that is, most of their assets were purchased with debt. Although highly leveraged, they also have to put up some of their own money as collateral to back their trades. When uncertainty soars, as it has under Trump, these highly-leveraged hedge funds need to reduce their exposure to market volatility by selling assets. This drives the prices of assets on their balance sheet down, which in turn requires that they sell even more assets to further reduce their exposure.

By April 9, a week after the initial tariff announcement, market indicators were starting to look quite alarming. A full-on financial crisis seemed quite possible.

But then the Trump administration in effect intervened to limit the damage. It didn’t lend money to hedge funds or buy troubled assets. But on April 9 Trump drastically changed his tariff plan, reportedly at the urging of his Treasury and Commerce secretaries, who were worried about the markets.

Economists who did the math on the new tariff plan didn’t consider it much if any better than the old plan, but investors saw it as a step toward sanity, and its initial effect was similar to that of a financial rescue operation. Markets didn’t go back to normal, and the dollar didn’t recover at all, but indicators of financial stress partially receded.

It’s not at all safe to assume that this is the end of the story. Details about how policy changed are terrifying rather than reassuring. Apparently Scott Bessent and Howard Lutnick persuaded Trump to change his policy by marching into the Oval Office while Peter Navarro, his tariff czar, was in another meeting. It’s easy to imagine the financial crisis coming back to a boil, and hard to trust that the crisis would be handled well.

As I said at the beginning, the outlook remains unclear. But even if Trump officials have managed to head off the full-on financial crisis that seemed all too possible 10 days ago, we still face a combination of destructive tariffs and a major loss of investor confidence in America. Not to mention foreign retaliation to those tariffs, completely irresponsible tax cuts, and general chaos in governing. I don’t think markets have fully internalized how bad it may get.

And we still have three years and nine months to go.

Write a comment